A Covid Hangover

If you were forwarded this post, you can sign up here.

When I was an adult, I asked my father––a tall, lean man with a shock of white hair–– how he invested money when I was a kid. His answer was simple: he didn’t. In part, this was probably because the markets didn’t interest him. In part, I suspect this was because he grew up during the Great Depression. For him, stocks losing 90% of their value wasn’t an aberration, it was life.

The point: the economic and psychological consequences of big shocks can last.

It’s hard to realize the Covid shock is of similar magnitude––almost 4 million dead––to other major historical shocks. Sometimes Covid doesn’t feel significant. I spent most of the pandemic in a suburban house. No one can say with precision what the Covid aftershocks will be. I do, however, suspect that trying to predict the recovery via classic economic analysis won’t work well because such models don’t factor in psychological shifts.

A bit of context (skip if you are a markets person). Economies tend to grow over time. When they grow very quickly, shortages develop and prices rise, which is called inflation. When they grow slowly surpluses develop, which causes deflation. Inflation shifts have a big impact on your wealth and, ultimately, happiness, a bit like how small shifts in the globe’s temperature have big impacts on the weather. When inflation increases quickly, your ability to buy things goes down. When this happens, typically (not always) central banks reduce the amount of money they are printing and this change then causes the assets you likely own, like stocks and real estate, to lose value.

On Wall Street, there is general agreement the economy will pick up and sharp disagreement about inflation. Those who believe we will get inflation are looking at Covid as a classic economic shock. We spent less, soon we will spend more, there will be additional fiscal stimulus and, presto, the economy will be growing so quickly we get inflation that is more than a quick burst.

That could happen. However, when I look at shocks I’ve witnessed first-hand, it seems to me they operate more like how my father did; there is an accompanying, sometimes counter-intuitive, psychological shock that impacts the economy and sometimes politics, too. A few examples.

a) The 2008 credit crisis. In its wake, a generation shifted their attitude toward the attractiveness of home ownership. This didn’t make rational sense. Home prices fell so it was attractive to buy.

b) 9/11. The day after, I recall watching fighter jets patrol the skies like angry wasps. Congress signed off on wars costing $6 trillion dollars, a massive capital misallocation relative to making investments in domestic infrastructure and education that could have boosted US productivity.

c) The collapse of Soviet Communism. Rather than lead to a global opening up, it eventually led to a turning in. Moscow and Beijing focused more on the subsequent fall in Russian living standards and life expectancy than the benefits of what proved to be a temporary expansion of civil liberties.

In the data, there are signs of a similar psychological shift this time. No one data point is predicative, the cluster suggestive. This makes sense. Our wiring hasn’t changed. Disruption changes us.

Elevated savings rates. Savings rates, how much of each dollar is spent versus saved, have risen above average. It may reflect stimulus checks, it may also reflect a recognition that life is uncertain.

China’s muted recovery. China has been ahead; it got the virus first, locked down more strictly and got out first. Yet, the recovery there has been modest, which recent forward-looking data shows. Of course, Beijing has not been nearly as stimulative as the US, so this is also likely muting China’s recovery.

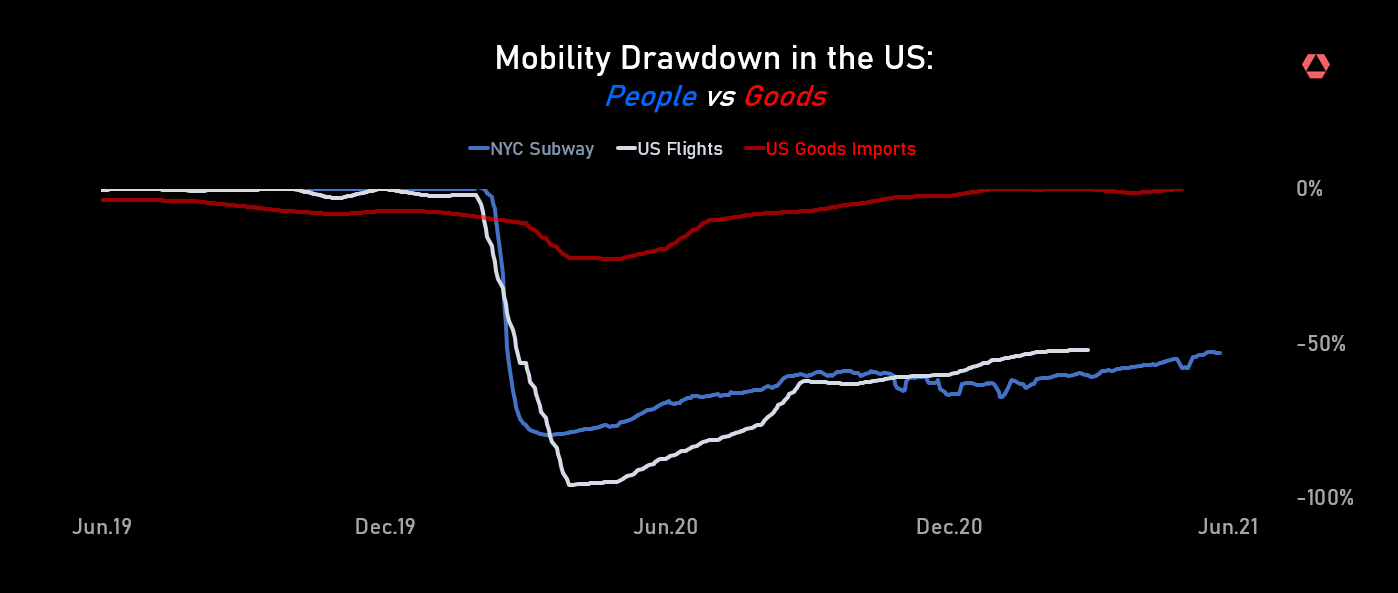

Tepid travel recovery. For every $100 spent in the global economy, about $8-$10 of it comes from travel and tourism. Yes, only about 20% of the world is vaccinated and travel restrictions exist, but perhaps there is simply more caution about being far from home, as the chart from Rose illustrates so well below.

Financial markets. Financial markets are not reliably predictive. That said, the bond market continues to predict weak growth.

In short, there are hints Covid is leading to behavior shifts, a bit like what happened with my father. By the way, his investment strategy was a mistake. He was applying a lesson learned in the 1930s to a very different reality.

Shifts in economics can in turn drive politics. Beyond economic caution, could Covid also make us more tribal? There is now a class of monied worker whose income is no longer tied to a specific community or workplace. The gap between these people––nomadic algorithm writers––and less educated, anti-vaxers is already a chasm and may widen yet further. That’s not good for political stability. At the same time, cracking down on tech monopolies to narrow this gap seems risky. How would we have survived Covid without Amazon?

In response to all this, I have modestly shifted my asset allocation—I’ve reduced the size of my hedges against a rapid Fed tightening and own a bit more stocks (though this letter is not investment advice).

If you enjoyed this post, please share with others!