If someone forwarded this to you, you can read this post to understand what Things I Didn’t Learn in School is about. Today’s post is free. Next week’s will only be for subscribers. A number of you have already signed up. Thank you. I am going paid for a number of reasons. First, I have a small staff and I want to pay them more. Second, after years managing money, I am trying to figure out if there is value in translating an investor’s thinking to a generalist audience. Putting a price on this information helps clarify that question.

I was sitting on a plastic chair drinking a coffee, staring at a brown river and taking in the last days of summer.

A Things I Didn’t Learn in School subscriber sat opposite and asked a deceptively simple question.

I’m reading your posts, he said, if you boil it all down, what’s the take-away?

Good question. That’s one reason I like writing. It creates quality dialogue. My answer is that we are in a bit of a lull. The forces driving stocks, bonds and house prices up are beginning to recede but only ever so slightly. There are very significant risks on the horizon, but so far they are not imminent.

However, the question triggered two reflections. First, these posts talk about pieces of the puzzle, like inflation or geopolitical shifts, but so far I have not shared an overall synthesis. Second, perhaps more useful than any synthesis, which will evolve, is the framework I use to generate a synthesis, which is what I will share today. In the follow up post next week, I will apply the framework to current conditions.

The markets are a bit like the weather; complex forces are at work even if conditions on a given day are relatively ideal, sunny with low humidity. Then an enormous number of small variables interact and suddenly it is hailing and everyone wonders what happened. Moreover, many of these variables have technical names that obscures their meaning.

When I was starting out as in investor in the 1990s and I was trying to figure out what was true, I had the chance to talk to George Soros. For reasons that were never quite clear to me, the chief of the bank I worked at refused an invitation to appear at special international CEO-only meetings. Through some Rube Goldberg corporate process, the invite was refused enough times that it ended up on my desk and I went in the CEO’s stead, whereupon I came into contact with Soros.

Soros tried to outline his philosophy in The Alchemy of Finance. I say tried because the writing is passionate, heartfelt and convoluted. His key idea is that markets are riddled with self-reinforcing processes. I believe this is both profound and true. Soros used the term “reflexive.” For instance, if you buy a stock, all else equal, the price rises. Seeing the price go up affirms your hypothesis and often makes both you and others like the stock more even though the stock is now, logically, more expensive and a worse investment when measured in terms of expected return. In this way, perception diverges from reality.

With that in mind, a stripped down framework for answering the reader’s question.

The economy and financial markets are logically distinct and inter-relate. For instance, when stocks go up, people who own them feel wealthier and spend more. When they fall the opposite happens. When assets fall a lot, like in the 1929 Depression or the 2008 credit crises, the psychological scars last a long time, decades.

When people say the “economy” or “GDP” they mean spending. GDP doesn’t measure many things that matter, like happiness or integrity.

Spending equals income plus borrowing times how many people exist, which is called population growth or demographics.

Income varies by sector (barber versus doctor) and is largely a function of both the rarity of the skill (brain surgeon) and output, which is called productivity.

Technology boosts productivity. If a farmer replaces a horse with a tractor, output rises. Technological change is self-reinforcing. One invention, an iPhone, allows other inventions, like Waze.

Borrowing is spending tomorrow’s income today. Taking on debt boosts wealth (a spiffy house) and simultaneously creates a financial vulnerability, the need to repay a known obligation (debt) with a variable source (income).

A growing population is self-reinforcingly positive for economic growth (more babies=more spending) and a shrinking population the opposite. Countries attractive to immigrants are structurally advantaged relative to those that are not.

If you earn more than you spend, you save.

Financial markets, or capital markets, connect savers with borrowers. The farmer needs to borrow to buy the tractor and the person with idle capital wants to lend and make a return. Capital markets are self-reinforcingly positive for wealth, which is one reason why places that did not develop them, like the Soviet Union, collapsed. If capital markets become too volatile, they lead to chaos, like Weimar Germany.

There are different ways to borrow and lend money, each with different advantages and disadvantages to borrower and saver. For instance, a stock allows a company to raise money without being obligated to repay it but also requires them to forfeit a degree of control. An investor combines assets into a portfolio with the goal of earning a return that is more reliable in aggregate than any single asset in isolation.

Every asset price is an expectation. Apple’s stock price today includes expectations about how many iPhones will be sold later. If those expectations are too high investors will lose money and vice versa.

Assets price relative to each other. If the yield (interest rate) on cash is high, investors will be more reluctant to endure the volatility of the stock market. If the yield is low, they might.

You can’t have economic activity without money; the government prints the money. (Bitcoin and gold are exceptions, a separate story).

By determining the supply of money, the government determines its yield, like the interest rate earned on holding cash in your bank account.

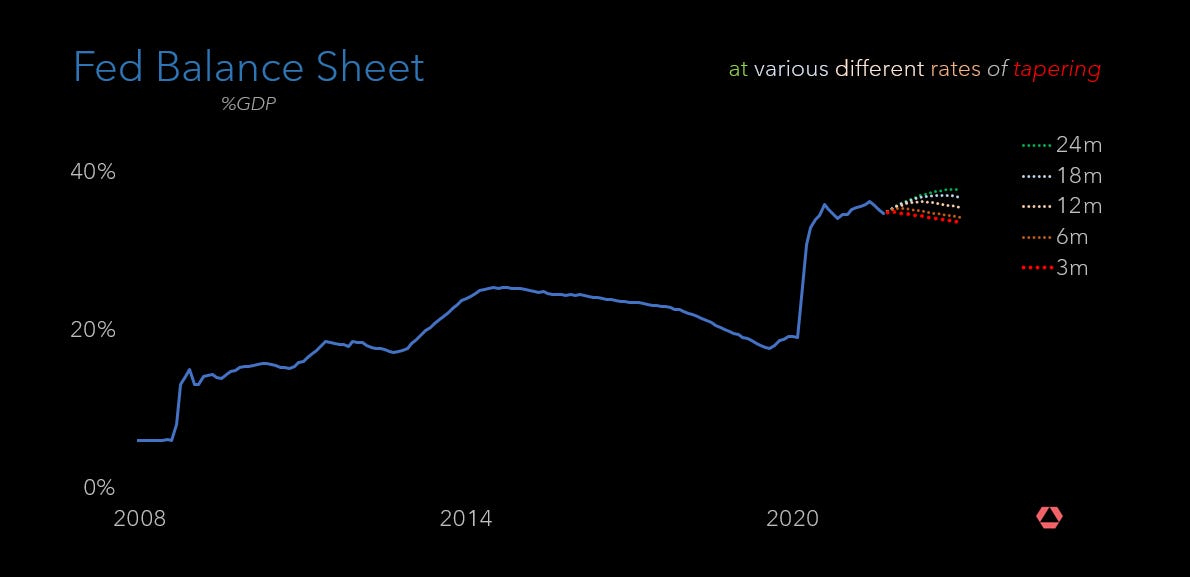

In general, assets go up when the government creates more money and fall when the opposite happens and, to foreshadow next week’s post, governments have been printing a lot of money and soon will begin to print less, as the chart from Rose Technology shows. The more assets rise the greater the economic sensitivity to their fall.

Thank you Paul for summarizing these basic concepts of financial marekt. Sometimes we immerse ourselves in it for too long and forget these, and we need to look at them from time to time.