Big Forces, Asset Pricing

Macro and Micro

NOTHING BELOW IS INVESTMENT ADVICE. INVESTING IS RISKY AND OFTEN PAINFUL, DO YOUR OWN RESEARCH.

“There is a lot of stuff going on…anything that is anywhere around physician judgement, what you see is…five to ten times more of recommended testing and surgeries than what you would normally expect from the literature.”

Nick Reber, Health Care Data Expert, on the podcast, here

Today I want to describe the big secular forces and scan relative valuation of assets.

I say the “big forces” with a recognition that truly big forces are often obscured. With the benefit of time, what matters becomes clear. However, we need to make decisions today, with our imperfect information and biases to overweight the recent past.

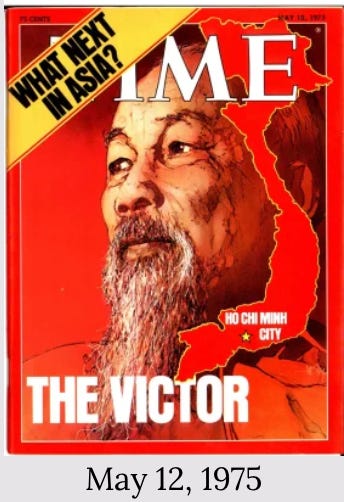

An example helps illustrate the challenge. When the US pulled out of Vietnam in 1975, the going logic was the US had committed a massive strategic blunder, impairing its global power, particularly in Asia. The cover below from Time illustrates the mood at the time.

In fact, in 1975 a revolution in computer chips combined with the growing manufacturing prowess in Taiwan, Hong Kong, Singapore and soon China was tying the US and Asia ever tighter and hardening the US lead in technology. The slow collapse of the Soviet Union likely began around this time because the shift in technology required not only knowledge about how to make a chip, but also how to mass produce them, at which the Soviet Union failed. Not a single Time cover in 1975 features chips because the shift was under the surface. We now know being a center of tech innovation was more important than losing in Vietnam.

Below are the big secular forces. The key question is how these forces translate onto the pricing of stocks and bonds, which is largely what we build a portfolio out of. The basic question is—-is the pie growing or not? If it is growing, how is it growing? The answer is that it isn’t growing too quickly and the growth is quite unequal, both in terms of who makes the money (tech, finance, energy) and where the money is made (disproportionately the US).

The key frameworks are:

a. output or economic growth = # of working people X productivity/person and

b. spending = income these people earn + borrowing against future income.

The forces:

AI. This is potentially a massive positive game changer for productivity. It is also likely deflationary. I suspect this is already boosting company earnings. One area that I can easily imagine this disrupting is medical care, which is in the stone ages, thus the quote from Nick Reber at the outset.

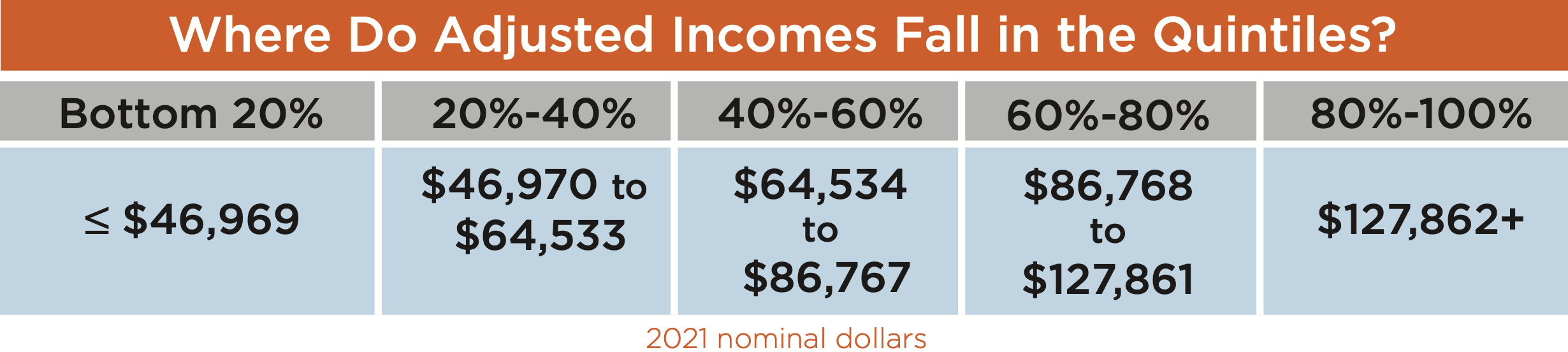

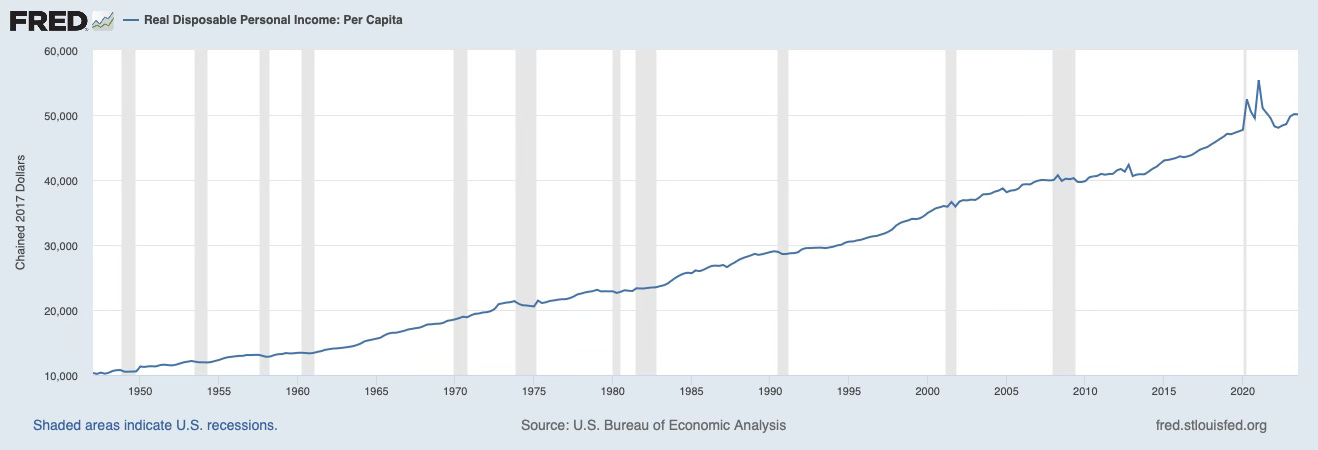

Wealth Inequality. The pie is growing due to tech and tech creates unprecedented economies of scale which then creates unprecedented wealth inequality, less because the poor are getting poorer (they are getting richer) but because their relative station is worse due to the enormous rewards that accrue to those people that are on the receiving end of scale economies. This is why Netflix CEO Reed Hastings ($4.5B) is far wealthier than Brad Pitt ($400 mln). Reed enjoys better scale. The lowest quintile in America today is far wealthier than most people were in the last half of the 20th century.