Inside a Georgian Kitchen (Take #2)

Inside a Georgian Kitchen (Take #2)

Podcast with Restauranteur Tamara Chubinidze

Oops! I earlier sent out a draft note without a live link and chart. Apologies. (Thus take #2).

Today Still Press published a podcast with Tamara Chubinidze. I met Tamara at her New York restaurant, Chama Mama. When I stepped inside, it brought back warm memories of both Tbilisi and a simple Georgian cafe in Moscow near Park Kylturi Metro I once frequented. The same way Croatia became a hot destination, I expect this is now occuring with Georgia. Tamara discusses her path, resilience and the power of food to convey not only culture, but love. I think you will enjoy this conversation.

The link (this time I won’t forget!) to the podcast is here.

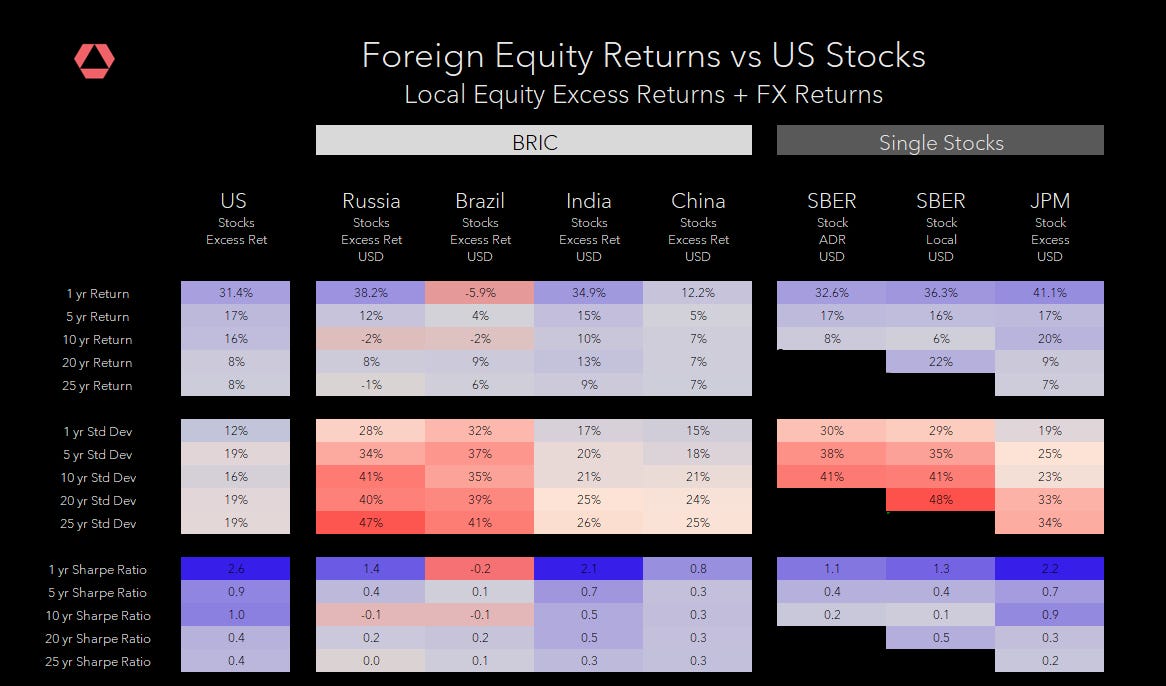

Separately, one reader questioned numbers in Sunday’s post Money Bad. The reader’s perspective was the return of Russian stocks since 2015 have been “humongous,” as the reader wrote. I cherish this type of feedback because it pushes both me and my partners at Rose to dig deeper. We went back and looked at the data again and below is a more granular picture of the relative return of US and emerging market stocks. These calculations are useful and not precise1. What looks like a wall of numbers matters a lot to finance nerds and investors.

What you can see based on Rose’s work is, yes, Russian stocks have done well recently BUT they are quite volatile, so volatile the return an investor gets for the risk they take is low compared not only to the US but many emerging markets. This return per unit risk (what’s labeled as a Sharp ratio) is a measure of an investment’s efficiency that is sort of like miles per gallon for a car. This doesn’t mean you can’t hold Russian or other EM stocks. It does mean though that you can’t prudently hold many of them and factually, over the long-term, the returns of a broad index have been poor.

Part of this volatility is due to the nature of Russia’s economy, which is highly dependent on a volatile source of income, oil. But part of it is likely because political risk rattles both domestic and foreign investors. This will not be picked up by looking at flows because you can’t measure an event that did not occur. Certainly the possibility of invading Ukraine doesn’t help.

Volatility exacts a significant toll on growing wealth. The classic example is having a $100 portfolio and losing 50%. Once your capital has shrunk you need a 100% return on the remaining $50 (ignoring compounding) to get back to where you started.

Other notes:

I will not be publishing Sunday, nor around the holidays in late December.

Lastly, I am raising prices to be closer to market and also to help drive investments in data and staff to make these even better. I had hoped to provide a warning on the price change but these calculations (above) took so long I ran out the clock. If there are students or others among you for whom the new price is an issue, reach out to me.

For those of you in the US, happy Thanksgiving. To the rest of you, we love our global audience. To all, we so much appreciate your support and interest in our venture.

-Paul and the rest of the Still Press team.

If you someone forwarded this to you, an explanation what we are up to is here and here.

The calculation includes the local stock market return and a forward currency return and gets trickier when prices are volatile and pricing unstable. It also doesn’t include transaction costs and fees, which probably make the returns look worse.