The tricky thing about investing is there are no fixed truths. There is common sense—buy low, sell high—but the game shifts because we shift. The market is people and our attitudes toward saving evolve, particularly after ruptures like depressions, wars and pandemics. This is evident in the “big quit;” millions of people suddenly leaving their salaried jobs, myself among them.

When I took this decision, I made some calculations. I will share them here, call it the cost of breaking free. Knowing these calculations shifts money from something emotional and mystical to something quite simple, like tracking calories.

My calculations differ from those of a typical Wall Street shop. Their calculations assume good things will happen, like that the stock market will rise. As a result of this assumption, they say you can spend down 4% of your savings every year. While it’s true that on average stock markets rise, it’s also true that they go through decade plus periods when they don’t and such a period could easily overlap with the time when you try to jail break. Don’t make optimistic assumptions, instead assume things will go badly and be pleasantly surprised if they don’t.

Here are the steps, along with a table and a calculator to let you do this yourself.

Step #1

The first calculation is the Steve Jobs calculation, which is the “knowing I will be dead soon,” as he described in his Stanford commencement speech. How soon? Find out.

I used the US social security administration actuarial tables, which suggest those of us in the US will generally be dead by age 85. By this measure, I have about 370 months left to live. Of course, there is a wide band around that mid-point. I put that band under the category or refinements (more on that below).

I suspect the pandemic forced people to consider their own mortality. Perhaps it also showed an alternative way of living. Many of you probably have some dream. Maybe it is starting a company or living in Italy or running for office or starting a family. If it’s holding the salaried job you hold, fine. If it isn’t, apply the Steve Jobs test.

Step #2

Know your run-rate, how much money you spend each month. You can drive yourself crazy trying to figure out this number. Don’t. A very rough estimate will do.

The big thing you spend money on is the obvious stuff, like taxes, insurance, shelter, food, etc. Each month track roughly what you spend. Write it down. Average this over a few months and you roughly know your run rate. You can also ask others how much they spend.

Recognize this is what you spend after taxes. The typical US family spends $5000 a month. To keep it simple, round up and assume they spend $100k year or a bit more than $8000 a month. That means they’d need about $130k a year pre-tax. The more they spend the higher the tax bracket and vice versa. Just like you want to under-estimate investment returns you want to over-estimate your spending.

The lower this run-rate, the easier it is to break free. That said, you need to make BIG changes to make a difference. Switching from a latte to a black coffee won’t move the needle. Moving from New England to Mexico, avoiding addiction or a messy divorce will.

Step #3

Multiply months left to live times your expenses. Take the $100k a year spending person with 370 months as an example. They need about $3.5 million saved to break free. Adjust this number down for money already saved and up for debt owed.

If these calculations seem simple, people aren’t doing them. The typical US family has about $100k in savings. This is in part because in the US there is not forced savings, a contrast to an Australia where there is. I think asking the average American to figure this out is quite a stretch. Maybe this essay can help.

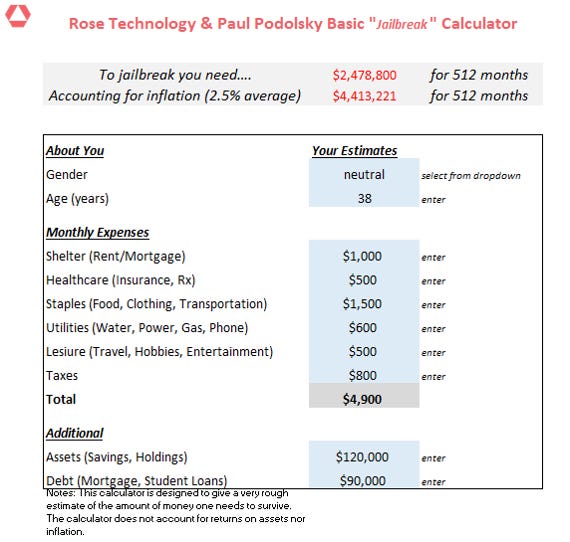

A sample table looks like this.

Here is a calculator you can play around with this yourself, one in Google sheets (thanks my friends at Rose!) and one in excel.

Google sheets:

https://www.dropbox.com/s/81ncrbsiazfokbn/cost.of.jailbreak.calculator.v2.xlsx?dl=0

Excel:

https://www.dropbox.com/s/81ncrbsiazfokbn/cost.of.jailbreak.calculator.v2.xlsx?dl=0

To make the analysis more precise you can:

a) Adjust the lifespan, i.e. if you don’t smoke you live longer.

b) Adjust income. How profitable will your break free occupation be? I assumed I’d earn zero. Too pessimistic?

c) Adjust inflation. This is a biggie. To be more accurate, assume expenses grow by the rate of inflation. That will make this analysis look even worse. Inflation is discounted to be about 2.5% a year over the next 10 years.

d) Assume asset growth. Asset prices do indeed rise over time, on average. This would make this analysis look better but given 7% current inflation, they need to rise a lot.

e) Include social security and Medicare. In the US, once these kick in, expenses fall.

f) Jail break without the cushion, recognizing that you are taking a bigger risk.

Other:

Market views:

Since I’ve started this newsletter, I’ve made three big decisions: avoid bitcoin, sell bonds and buy stocks. Since the time I shared those decisions in print, bitcoin is down 25%, bonds have lost about 4% and the S&P is up 22%. These essays are not investment advice; I am sharing with subscribers what I do, when I do it. I am moving around my portfolio more and will update that for subscribers later this quarter.

What I’m reading:

Non-fiction: Unique, the New Science of Human Individuality, by David Linden and Morality, by Jonathan Sachs. David published an essay in the Atlantic that struck me. “It is possible, even easy, to occupy two seemingly contradictory mental states at the same time.” Agreed.

Sachs argued the foundation of “civil society,” the sphere independent of politics and business, was anchored by a Judeo-Christian moral framework that believed in absolute, not relative truth. He argued that as this code weakened, society became more fragile.

Fiction: The Age of Innocence, Edith Wharton; Les Misérables, Victor Hugo. These are old classics and remind me both how much and how little things have changed. One of Hugo’s characters says that the important question is “how to create wealth and how to distribute it.” Many nations are having that same debate now. That’s evidence in the US and also China’s “common prosperity” push.

It is minus 9 outside today…time to go for a ski. Talk to you next week. Write with questions…I can arrange calls with subscribers.