Moral Man, Amoral Markets

If someone forwarded this to you, you can sign up here.

Come on man, we are surrounding the administration building, let’s go, said a guy with curly hair in a jeans jacket.

I was sitting on a college green. As I recall, it was a crisp fall day in 1986 in Providence, Rhode Island. I was a freshman.

What for? I asked.

To get them out of South Africa.

Thus began my first interaction with what has come to be known as “impact” investing, the notion that one should weigh ethical considerations in investment decisions. The jeans jacket guy was referring to the university’s endowment.

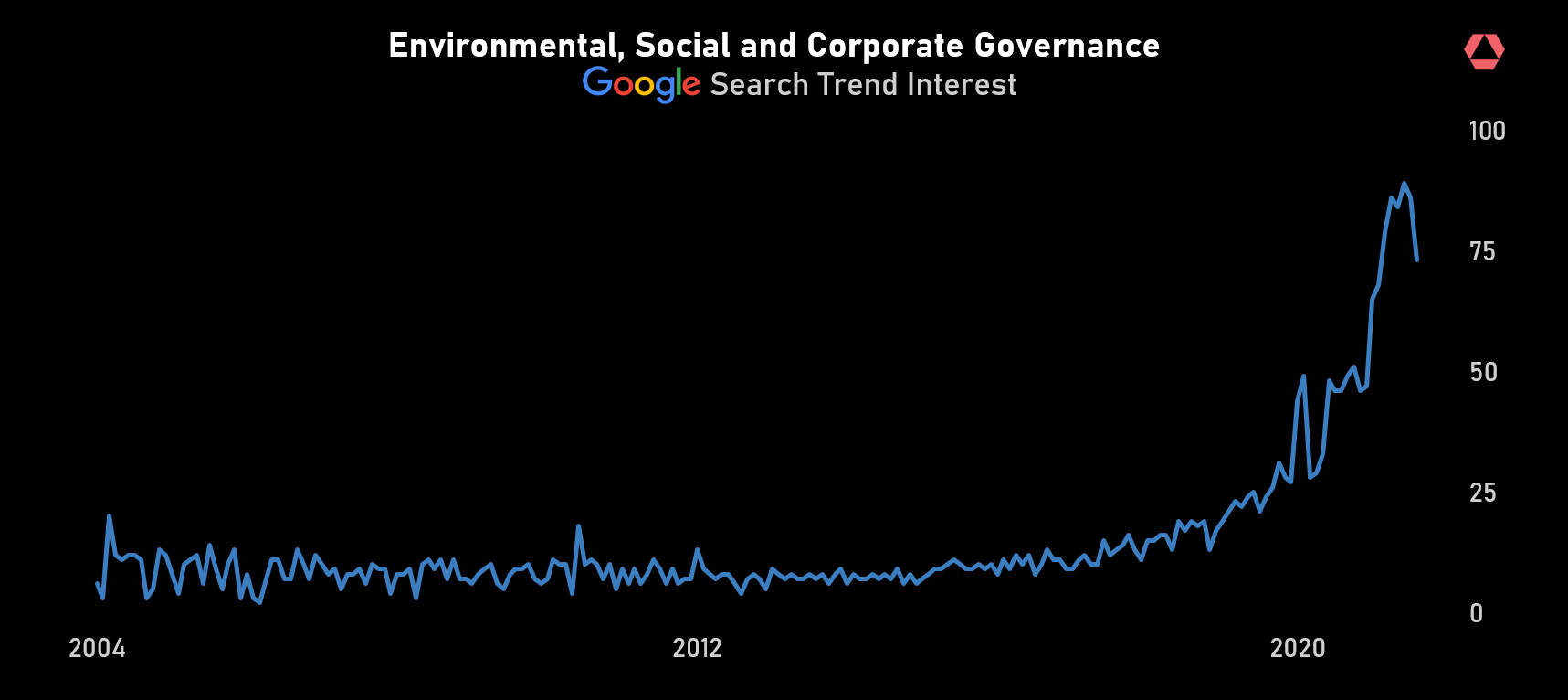

In different ways, this idea continues to ripple through financial markets. Last month, Bloomberg reported that ESG—Environmental Social and Governance investing—had reached $50 trillion in assets; last week, news outlets reported that credit card companies sought to distance themselves from the Only Fans website due to reputational concerns. Earlier this year, US government officials discouraged investors from holding bonds from US rivals, like Russia. Different flavors, same idea.

Ethics are the glue that encourage us to act from our better selves. In open societies, they are also reflected in a political process where these notions translate into rules we agree to live by. It was this process that led to substantial (and obviously overdue) legislative shifts like outlawing slavery in 1865 or the Civil Rights Act of 1964. The political process is arduous in part because notions of good and bad are both unstable and debatable, meaning the vision of the idealized society we are striving toward evolves. Impact investing is to supposed to hasten this journey, which sounds alluringly noble but in practice may well lead to worse outcomes.

Unlike politics, investing has measurable goals. Over time, the goal is to channel current savings into productive future investments. This is measured by productivity, or output per person. The goal of capital markets is to price this resource allocation. From an investor perspective, the goal is to grow money as much as possible while enduring the lowest possible risk of loss. This ratio of return to risk is how investment managers measure themselves.

The higher the ratio, the better the result. Think of this ratio like miles per gallon. I’ve tracked my ratio over time. While the majority of my investment ideas work out, some don’t. I get a lot of things wrong. This is normal, but I don’t want to make the game harder than it already is by adding additional complexity.

Predicting return and risk is difficult, almost impossible. A pandemic comes along and predictions turn out to be wildly off. Companies that were thought to be relatively safe, like airplane or hotel companies, suddenly become risky. The list of disruptions is long––pandemics, new technologies, wars, financial crises, etc. This is why I try to keep my investment assumptions, like diet guidelines, very simple, as I’ve explained previously.

Impact investing introduces a third variable. With regards to ESG, there is a complex rating methodology for each asset. Embedded within the rating system is the political question cited earlier, our vision of an idealized future. Given how hard it is to get the first two variables—risk and return—right, I am skeptical adding a third variable that purports to accurately calculate the relative ethical impact of a tobacco company to an oil company will help.

Moreover, if I exclude certain assets from the potential pool of investments, which is what that protestor was arguing for in 1986, several things happen at once. First, I lose the ability to influence an outcome, like using share ownership to encourage a company to shift hiring practices. Second, I impair my ability to create a diversified portfolio, leading to higher risk portfolio concentrated in certain sectors. Third, I may incur higher fees. Fourth, I impair the ability to distill market pricing.

This last element is likely esoteric for non-investment people, but it is important. Financial markets offer perspective on what investors believe the future course of growth, inflation, credit risks and other measures will be. Policy makers, like the central bank, use this information to adjust course. Withdrawing from markets, like forbidding investors to hold Chinese or Russian bonds, undermines this process.

I have other questions. If we are truly concerned about, say, the environment, isn’t the best thing to simply consume less? That’s terrible for the stock market and impactful for the environment. If there are things I am missing, I genuinely look forward to readers educating me. For now, impact investing isn’t part of my strategy. In terms of my asset allocation, I continue to be long stocks, raw materials and bonds outside the US. I still have hedges against Fed rate hikes, but they are smaller than they once were.

Note: next week, season 3 of the Things I Didn’t Learn in School Podcast comes out. Look for an email like this with an intro and a link.