Oz, Tornados and Limits

Oz, Tornados and Limits

Real Yields Are the Force Behind the Force

If you are new, welcome! The idea behind these posts is to connect big picture macro and little picture micro. Macro is history, technology and the economy. Micro is emotion and personal journey. I’m trying to integrate often siloed worlds. My first book, Raising a Thief, and podcast on Apple Podcasts and Spotify are micro. These posts are macro but it is all one thing—making sense of what is going on around us. Most of this content is free. It takes a team to build this and I thank all my paid subscribers for your support. Enjoy.

Modern life offers both unprecedented comfort and complexity. Humans haven't changed but our world has. We can only hold so much in our heads and are prone to bouts of optimism and despair. The combination of our mental limits and the world’s increasing complexity makes understanding harder.

When it comes to money, some readers tell me it is now too painful to look. Why exactly is wealth disappearing? Inflation is over 8% and the stock market down 18%. Stocks, bonds and confidence are falling because the real interest rate (shown below), has risen from -1% to a bit above zero. Yet, outside of bond traders, no one knows what a real interest rate is, why it matters and how it works. But the real interest rate is nothing new.

I know bonds bore most people as much as good drama intrigues them. To circumnavigate our resistance to the abstract, parables tap into our predilection for story. The most famous money parable in the US is The Wizard of Oz, the Bridgerton of 1900. To refresh your memory, Dorothy is swept up in a tornado and finds herself on a yellow brick road with a scarecrow, tin man and lion battling a terrifying witch, all while searching for the Wizard.

How much the symbolism was intended isn’t clear, but it doesn’t take much of a leap to create it. Dorothy = midwestern goodness, yellow brick = gold, scarecrow = farmer, tin man = industrialist, Oz = ounce. The wizard is the person who decides how much money to print.

Past Symbolism Echoes Today’s Politics

When The Wizard of Oz came out, about 40% of the US population were farmers. There was no Federal Reserve. It was created in 1913. Now 1% of the population are farmers and the big money is in technology and finance, not agriculture and industry. We still struggle with deciding how much money to print, however.

The Wizard of Oz’s publication followed a Presidential race where the big issue was whether the US should remain on the gold standard or switch to a gold/silver or “bi-metallic” standard. Back then, people believed a dollar of currency should be backed by something tangible as opposed to a loose promise from the “Emerald City.” Gold couldn’t be printed, was rare and durable. This meant the money supply expanded and contracted not due to human judgement, but by how much gold was discovered. California gold rush meant money supply expanded.

Bi-metal meant more money (backed by gold and silver), so more printing. In 1896, the Democrats wanted more printing, the Republicans wanted less. McKinley, the Republican candidate, won and the US stayed on the gold standard. Today a technocrat, Powell, is supposed to decide how much to print even though a politician, Biden, will be blamed for inflation because, like I said, no one knows what a real interest rate is.

Winners and Losers

The real interest rate is the cost of money. If you print more, the rate falls. If you print less, the rate rises. The real interest rate drives nominal interest rates, mortgage and corporate borrowing rates and PEs, the price one pays for stocks. In other words, it drives everything. This is why financial people pay more attention to the central bank than Congress.

If you print too much, you get inflation. If you print too little, a depression. Neither is desirable and in either scenario there are winners and losers. The challenge is adjusting policy such that the wins and losses are tolerable. When inflation spins out of control, like in Weimar Germany, it leads to huge shifts in wealth and political instability. Today’s 8% inflation qualifies as out-of-control, though I suspect it will begin to come down.

Traditionally, higher inflation favors debtors, because the real (inflation adjusted) cost of debt falls, and hurts lenders, who are getting paid back in now increasingly less valuable money. Deflation is the opposite. If the economy is collapsing and you are collecting 5%, 6% or 7%, your ability to buy improves.

In the The Wizard of Oz, the agricultural and industrial interests—the scarecrow and the tin man—are dependent on credit and would benefit from easier policy. The wicked witch of the east, perhaps a stand-in for banking interests, not so much. Today, the winners and losers are different. The winners are commodity producers and the losers are tech and the consumer.

Tech’s Free Money

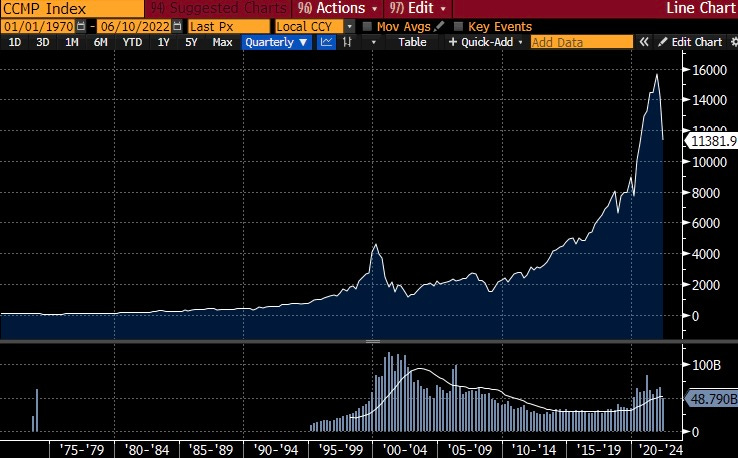

Dorothy is swept up in a tornado. We were swept up in a pandemic. When the pandemic struck, demand collapsed and so did inflation. So the Fed printed a lot of money to replace the spending consumers were no longer doing. With bonds yielding nothing, money poured into stocks, driving up the price of tech stocks in particular, as shown below. If tech stocks revert to pre-pandemic levels, they will decline another 20%.

This pop in tech stocks was the final stage of what has been a protracted shift. Years of low inflation created a self-reinforcing loop. Companies with novel if unprofitable ideas could fund themselves by selling stocks to willing investors.

Companies like Uber or Twitter became familiar to many even though they didn’t actually make money. Investors were excited because these companies, theoretically, offered enormous economies of scale. As opposed to owning a taxi company in New York City, you could own technology that drove taxis all over the world, without paying for the taxi. But the secret to this magic trick was persistently falling real interest rates, the force behind the force, which created an insatiable appetite for stocks.

As I wrote last week, while consumers initially benefited, producers and traditional gate keepers (like fact checkers) get hurt. I estimate Amazon has caused a roughly 70% deflation in book prices and there is clearly some more difficult to quantify pass through to our civic culture. Senate Bill 2992, the America Innovation and Choice Online Act tries to tip the balance away from distributors like Amazon toward producers, possibly hurting consumers.

Disruption is how capitalism works. But disruption is different than a bubble. The collapse in real interest rates inadvertently further boosted the prospects of already powerful tech giants and simultaneously helped create so much inflation that consumers are now solidly on the losing end. Now the unwind is underway.

Bond Traders Versus Tech Investors

Tech investors and bond traders think differently. Palo Alto likes novel visions of the future. Much of this turns out to be bunk, a small portion miraculous. For instance, companies have been trying to figure out how to have a computer replace a secretary in a way that doesn’t make a caller homicidal for at least thirty years and have so far failed to succeed.

To be sure, it is true that the computer I am writing this on is powered by insanely fast chips allowing me to pull in information from all over the world and video chat, for free, anyone I wish. That’s something and these innovations are fueled by the stock market. Ditto mRNA vaccines.

Bond traders see the world in terms of limits. The economy can only grow so fast, oscillating between a few percentage points positive to a few percentage points negative. This speed limit is determined by a) population growth and b) productivity, how inventive we are.

Real interest rates are tied to this speed limit on growth. The real interest rate is the nominal interest rate minus inflation. Typically, the real interest rate can only get so high, when money is tight, or so low, when money is easy. During the pandemic, things got out of balance, real interest rates plummeted. Could the Fed now lose credibility? Yes. In bond trader parlance the “tails” become more likely in this dynamic, which is to say low probability events become more probable.

Commodities and Strangling the US Economy

Inflation is the average price of a pile of stuff. Some of that is tied to the US, like the cost of hiring a person, but some of it is not, like oil and the price of imports, many of which come from China. Putin invading Ukraine disrupted both wheat and oil, leading to an explosion in prices which will now create an enormous pay day for those who can produce or transport what Russia no longer can.

Similarly, Xi’s zero Covid policy is continuing to snarl ship traffic, leading to goods inflation, as the Rose chart below shows. Some of my Shanghai readers will, as I understand it, be submitting to another round of mandatory testing Saturday. Note how all prices are up but goods (from China) and energy lead the way.

The Fed needs to stop the inflation and it only has blunt tools to do it, interest rates. It can not influence Putin or Xi. What it can do is strangle the US economy.

How much do they need to strangle the US economy? The US economy can run, without inflation at about 2% growth a year, 1% due to population growth and 1% due to productivity improvements (what the tech is supposed to provide). That means the economy needs to run below 2% to get inflation to ease, maybe a lot below given that food and energy price shocks are coming from abroad. I suspect the US economy is already slowing quite a bit.

Investment Implications

At the end of Oz, they finally meet the Wizard. He turns out to be a guy just like everyone else, struggling to make sense of things and pull the right levers. We all are.

Keep reading with a 7-day free trial

Subscribe to Things I Didn't Learn in School to keep reading this post and get 7 days of free access to the full post archives.