The Dictatorship of Reality

Inflation, China and Policy Flubs

Note to readers: in addition to these posts and the podcast, I write books. Just before I publish a new book, I test it with beta readers. If you are interested in being one, give me a shout. The first book, Raising a Thief, was non-fiction. Book #2 is fiction.

Watching stocks sink and Xi support Putin’s war isn’t easy. But, if you value your autonomy, it’s better to watch and be alert to how they are connected. That’s true even if the money world bores you. Reality is a dictatorship.

The English writer Virginia Woolf said to write one needed a “room of one’s own.” “One’s own” has a literal meaning for a writer and a conceptual one for everyone else. It means having the money and autonomy to pursue your curiosity, whatever that may be. Because money is constantly unstable, we either pay attention or pay the price. High inflation is forcing the central bank to stop printing money, driving assets down. If Xi follows Putin’s lead, which seems increasingly likely, beyond the world becoming more scary, the inflation forcing the central banks to act will get worse. Rising inflation, falling growth and external challenges in turn increase the risk that open societies elect a dictator. As the Jan. 6 hearings show, the US already did.

Summary:

In response to surging inflation, central banks are rapidly pulling back on printing money, driving down all assets.

Inflation is exacerbated by war in Ukraine and climate change related drought, which together drive up energy and food prices. Because this is outside the control of central banks, they need to tighten even more.

China is indicating it intends to forcibly absorb Taiwan, though only Xi knows for sure. If this happened soon, it would significantly prolong current turmoil, including inflation.

In open societies, the combination of high inflation, weak growth/income disparity and external threats weaken confidence in rule-of-law systems, increasing the risk a dictator gains power.

Tightening and Wealth

Less money printing equals lower asset prices. It is that simple. As of this writing, the US stock market, in real, inflation adjusted terms, is off by almost 1/3 this year. Global stocks are all negative. Sooner or later, this hits you or people close to you via a lost job or diminished savings. If we all desire a “room of one’s own,” a contraction in asset prices makes achieving this more distant.

In markets, by the time something is obvious, it’s already at least part way over. Stage one in the stock market decline is the price one pay’s for a unit of earnings, or the PE ratio, falling. It’s gone from the low 20s to around 16, which is closer to average, as my previous posts have illustrated. Stage two is the earnings declining. If the stock market is tanking and the central bank is raising rates, earnings will soon get hit. I expect this will drive the stock market down yet further (NOT INVESTMENT ADVICE).

Of course, different sectors respond at different rates. Remember FAANG (Facebook, Amazon, Apple, Netflix, Google)? This was like the Nifty Fifty years before. Below is a chart of Apple, which Warren Buffet has a large position in and has only recently started to slide. Apple makes great products and it’s an expensive stock. Despite all the turmoil, the PE is around 20…it’s been as low as 10 in the not so distant past, meaning some stocks may see both falling PEs and earnings.

The Fed will start printing again when the economy rolls over, not before. The tech companies are already starting to fire people and soon this will show up in the employment numbers and the entire economy. But until inflation falls enough that the central bank can stop raising rates, the stock market will struggle. The chart below that Rose Technology created takes the average of every major stock market decline since 1957. The market never hits bottom until the Fed stops hiking and there is no risk of that happening soon.

Conflict and Inflation

Russia is trading its wealth for territory. Before it invaded Crimea in 2014, Russia had a growing economy, a near lock hold on many commodity exports (not just oil and natural gas but metals like palladium and aluminum) and an increasingly wealthy population. What cold go wrong?

The best news source for Russia, beyond looking at the economic data, are the documentaries from Alexei Navalny’s Anti-Corruption organization. They show how Russia actually works, which is why Navalny is in jail. The most recent documentary was released Thursday. It details obscene corruption at the natural gas giant Gazprom. The difference between oil rich Norway ($66k per capita) and oil rich Russia ($27k per capita) is graft. The 20-year return on Gazprom, the biggest natural gas producer in the world is….zero. (See my Twitter for chart).

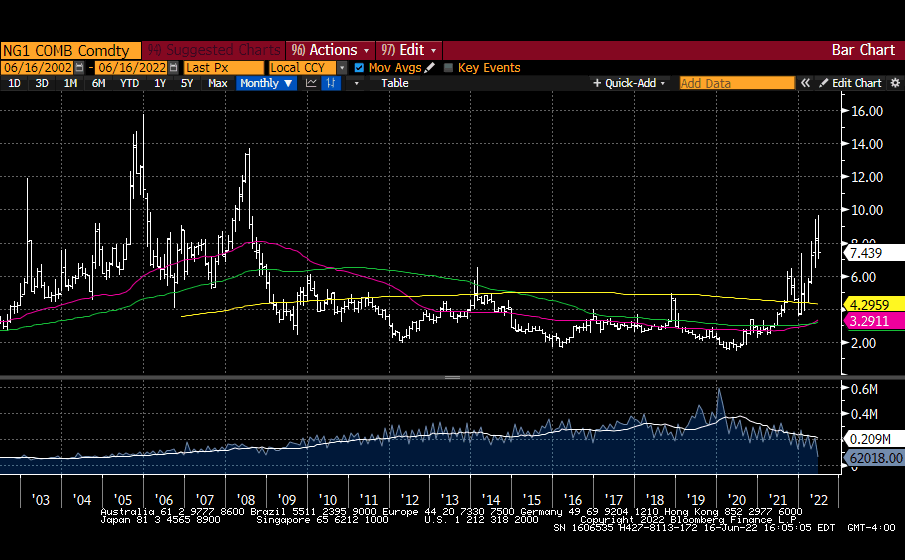

Now the West is trying to replace Russian oil and gas even as Russia counterattacks and cuts them off. Not surprisingly, gas prices have tripled. This is inflationary and makes the Fed’s job much harder.

China is commodities poor but production rich. This week, Xi defended Putin’s war (noting the “legitimacy” of Russia’s attack), unveiled a third aircraft carrier and China watchers like Bill Bishop highlighted a statement from the Cyberspace Administration citing the wisdom of Mao. Each week brings something like this. China invaded Vietnam in 1979 and if it does the same with Taiwan, the disruption in current supply chains will seem tiny. Inflation will shoot higher as the West, Japan and Australia level sanctions on China. Where will Apple make its phones?

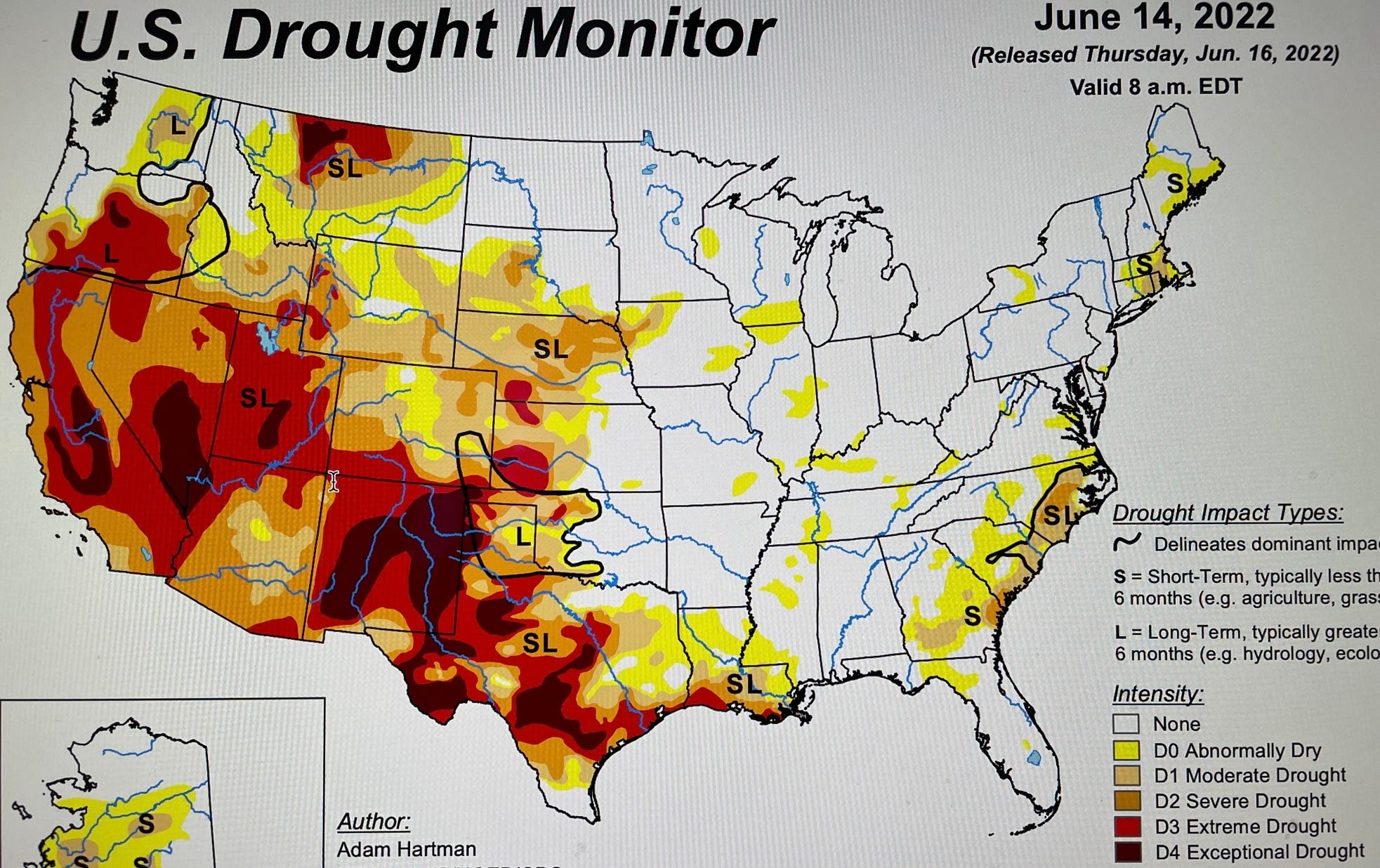

A final inflation image that deserves a separate post. High temperatures driven by global warming are creating drought and driving agriculture prices (food) higher. This is on top of the interruption in wheat exports from Ukraine. All this means the central bank may need to step on the brakes even harder, depending on the timing of all these disruptions.

Political Cost of Policy Errors and Dictator Risk

What brought us to this? It’s complicated. One vector is a string of policy errors. Some major flubs:

The Fed. The Fed messed up by not removing pandemic-related liquidity more quickly. This is the second big goof up this century, 2008 being the last. The major screw ups they’ve made before are 1929 and the 1970s.

Believing that the West could work with Putin and Xi. The big assumption in the West, including with me, was that as these countries became more commercial, they would be more peaceful. That’s clearly not true.

Climate change. A collective failure to move faster.

The FCC. This relates to a previous post, The Cacophony Economy. The 1934 Communications Act stipulated that radio and TV was in part a public good. The internet is immune from such rules, which is part of what has created a post-truth world.

I wonder if part of these errors isn’t a talent challenge. I’m told that the staffing has deteriorated at places like the Fed. An analyst at the New York Fed makes about $75k. A typical software engineer fresh out of school makes around $200k. Those people I know at the Fed are good souls and I wonder if government is drawing the requisite talent. My fear is high inflation, a sliding economy and external threats leave open societies vulnerable to dictators. The January 6 hearings show the US already had one who, miraculously, didn’t pull off what he wanted. Bad policy creates bad outcomes creates a lack of confidence in the system itself.

What Happens Next - Investment Implications