The Plot Shifts

Not investment advice.

We are in the midst of a violent repricing of relative cash flows amid AI and an erosion of US rule of law. No one fully understands how this new technology will end up working, including the people who make it, so when highly convicted sellers enter the market, others who would normally buy are scared and don’t step in—and stocks like Microsoft, below, drop a cool 20%. This drama is playing out across a complex terrain that can’t be separated from the institutional shifts.

In more detail:

Either the decline in stocks like Microsoft is an overreaction (possible) or many, many people are about to get fired. If MSFT is worth 20% less because their AI agents don’t measure up to Claude, then for sure some significant part of the 228,000 people who work there need to go.

If these people are let go—and they are certainly being let go in large numbers from Amazon, UPS, FedEx, and other companies that can automate/AI themselves to a smaller headcount—then inflationary pressures are ebbing… fast.

The labor market data is hard to parse because of the radical tilt in US immigration policy. On the face of it, however, the unemployment rate is falling and claims for unemployment insurance are not rising. This is possibly because an engineer fired from Amazon is not filing for unemployment while on severance, and these adjustments are happening quickly; it’s also probably because the workforce is shrinking. Soon the US will have labor force growth like China or Japan, which is deflationary. The jobs that are being created are in elder care.

There is no inflation, despite the AI capex spend. Below is a snapshot of CPI. Just as the politicians on the left and right are declaring new solutions to combat rising prices… prices have already fallen. CPI is a little high in outliers like the US (tariffs) and Australia (low productivity), but CPI is below two and closer to zero in Europe and China. An equal average of the three of them (China, US, Europe) is 1.7%, and if the US had not implemented tariffs, inflation would be even lower.

If the range of outcomes on stocks has widened (could my favorite company get destroyed by Claude?) and this technology is simultaneously accelerating technological disinflation, then the relative appeal of long-term bonds to stocks is rising. The return to risk ratio of stocks is going down because volatility is going up. So far this year, a 10-year US government bond is outperforming the S&P 500.

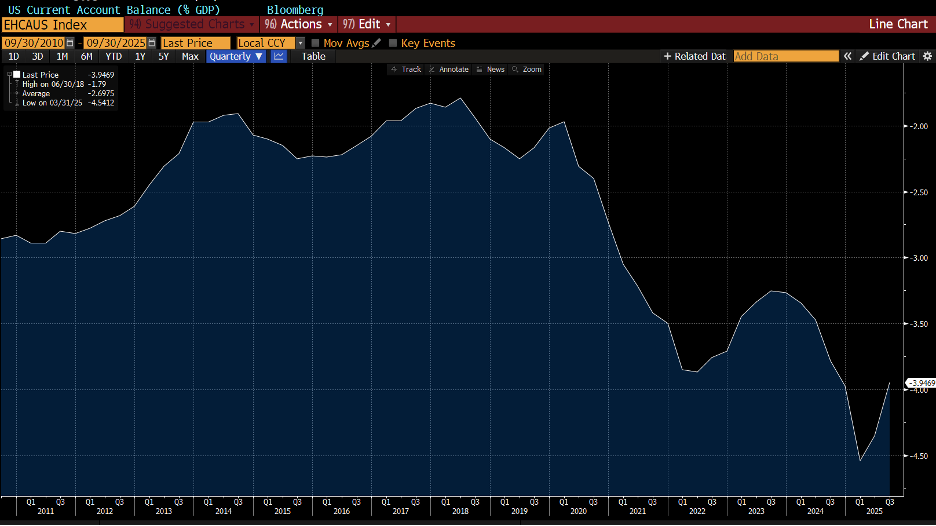

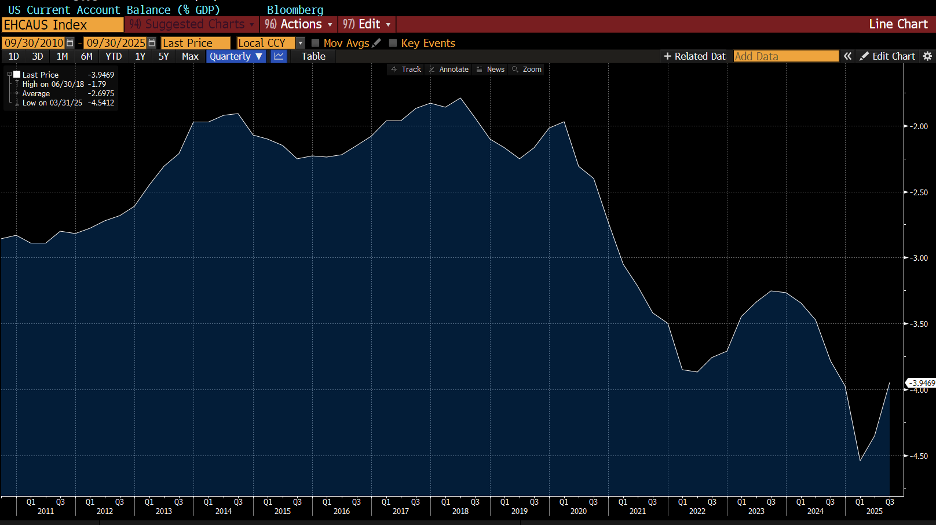

The other axis is foreign currency. The US needs to attract $1.2 trillion a year to keep the dollar stable. That’s what running a 4% current account deficit on a $32 trillion economy means. The reason the dollar has not gone down a lot more is because foreign investors like buying US tech stocks. But if US tech stocks stop going up, the dollar inflows grind to a halt or at a minimum slow. For the biggest savers, like the Japanese, the currency-hedged returns of buying US bonds are not attractive.

The “where to put your money” question gets even trickier when precious metals stop operating the way they once did. Because there is so much speculative money long metals, they trade in line with tech stocks as opposed to as a diversifying asset. Both fell sharply at the exact same time Thursday, in what looked like programmed selling.

Finally, Bitcoin. It cannot catch a bid. There is no intrinsic value in Bitcoin, and it appears to trade more in line with the White House popularity, which is to say not high. The simplest explanation is often the hardest to come by but most accurate. It seems a disruptive deflationary technology shock is unfolding at the same time as the US severs 80-year-old institutional linkages, and capital flows are in a messy rush to find a safe harbor. This is bullish for foreign stocks, US bonds and some foreign bonds, and foreign currencies—and bearish for US stocks and US short-term bonds.

"If the range of outcomes on stocks has widened (could my favorite company get destroyed by Claude?)"

- Underappreciated dynamic. Bubbles form during technology shifts because most stocks are priced as winners - and that can't be true in the aggregate.

"The other axis is foreign currency. The US needs to attract $1.2 trillion a year to keep the dollar stable. That’s what running a 4% current account deficit on a $32 trillion economy means."

- Why can't this be true: "the US runs a 4% capital account surplus and that must be offset with a 4% current account deficit to keep the dollar stable". Put another way, why does the BoP need to be framed in terms of the current account and not the capital account?

"The “where to put your money” question gets even trickier when precious metals stop operating the way they once did."

- Exactly. When a market’s price action decouples from its fundamental drivers, it’s a signal that flows have taken over and you either trade on flows or sit out - waiting for a flows-based washout or fundamental catalyst (macro regime shift) that breaks the temporary correlation.

Thanks for the note!

Do you know any bond-cash(or dividend stocks) like instruments that you view as attractive now vs US bond?

JPY seems to be on a way to appreciate more, but small carry is not really atractive here