The Talent Skedaddle

Tracking People Migration

If someone forwarded this to you, you can sign up here.

You thinking of leaving? I asked.

I am, he said, looking away thoughtfully.

I was speaking with a Russian CEO on a sun-drenched porch in Istria, Croatia, not far from Slovenia and Italy. The translucent Adriatic sparkled nearby. He was wondering aloud if the Baltics, where he is now based, is far enough away to keep him safe from Moscow’s reach.

The Kremlin’s heavy hand is once again scaring off talent, a long-standing tradition. One of my great grandfathers made a similar calculation over 100 years ago and quit Russia for Chicago. Abandoning a country is wrenching. It typically takes several generations for a family to regain its footing. The talent drain also puts those countries that suffer from it at a structural disadvantage.

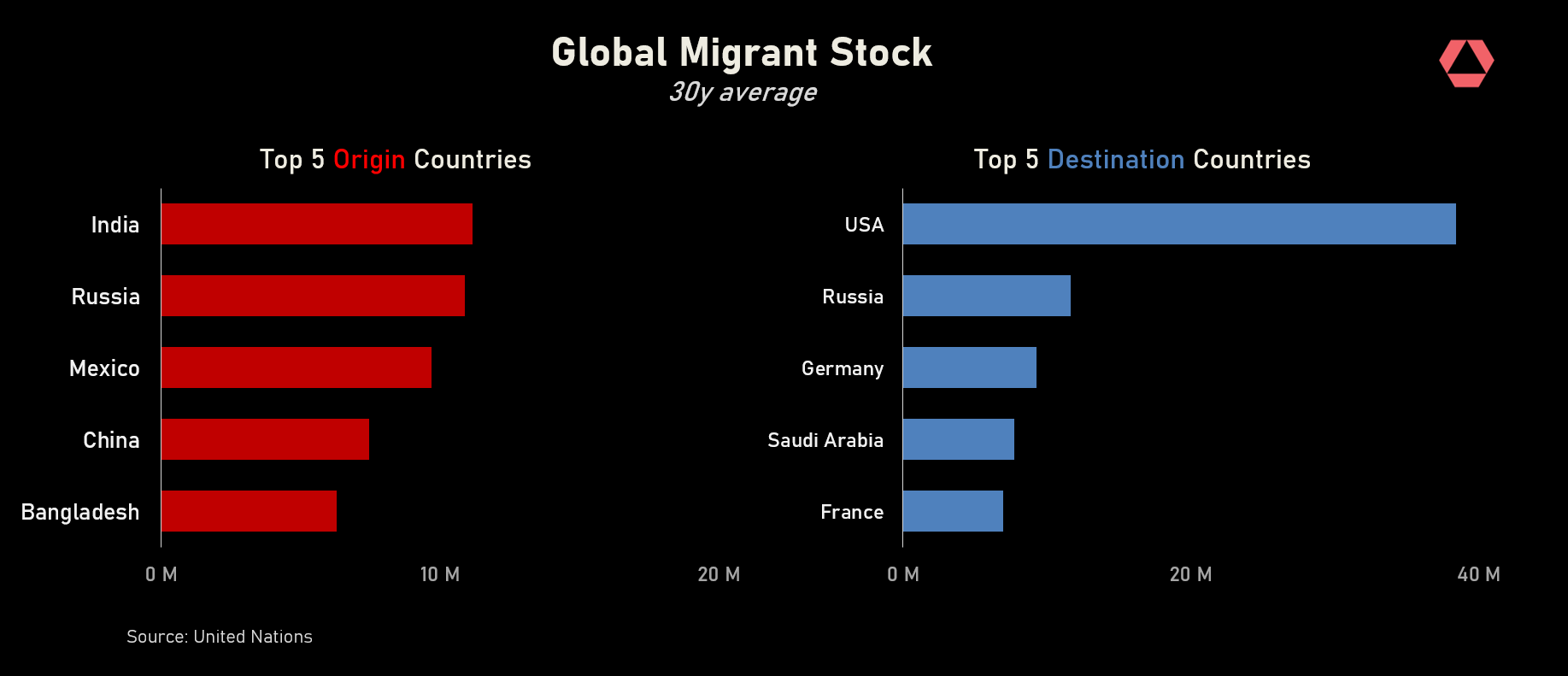

People skedaddle when they don’t feel safe and sense better opportunity elsewhere. Tracking this data provides an additional lens on both politics and markets. The data suggests that what investors refer to as “emerging markets” are seeing consistent people outflows in favor of developed markets.

That is unfolding even as dysfunction in developed markets is disconcertingly obvious. Pick your image––retreat from Kabul, bellowing anti-vaxers, storming the Capital, protest cities in flames, ballot recounts. Yet, as the chart below from Rose Technology shows, people are voting with their feet and looking past these concerns.

Russia shows up on both sides; people in Kazakstan and Uzbekistan find Russia comparatively attractive even as the educated Russian urban elite leaves. Saudi Arabia is reliant on immigrant labor from, among other places, Bangladesh.

Of the roughly 20 Russians I interacted with in Istria, over half hold foreign passports. The most recent twist that caught their attention is the Kremlin’s decision to label the independent media outlet “Rain” a foreign agent. Just as America can be divided into Trumpists and anti-Trumpers, Russia can be divided into the “Crimea Ours” camp (Crim Nash in Russian) who celebrate Putin’s Crimean seizure and those who are appalled by it. The “Crim Nash” group is in charge. China’s recent calls to focus on “common prosperity” are similarly ringing investor alarm bells.

Power and wealth are always in flux and the search for hospitable conditions is ancient. The Croatian town I am in has been claimed by Greeks, Goths, Romans, Venetians, Hapsburgs, Austrians, Italians and until relatively recently was part of Yugoslavia. We are animals and crave safety, particularly when we reproduce. As one Muscovite told me, “I worry not so much for myself, but for my kids.”

Most investors look at prices, not migratory data. From that perspective emerging markets like Russia and China are “cheap,” meaning what I’ve described above is already priced in. In fact, some investors currently believe these markets are too cheap.

Increasingly, I am not so sure. I like to put the price of all assets in yield terms, which allows easy comparison across stocks, bonds, real estate, etc. The current yield of the US stock market is around 3%. The yield on Russian and Chinese stocks is double that. Said differently, investors demand a higher return on capital to accept the risks of these markets. The question is whether this higher yield adequately compensates an investor for the risk.

While investing in emerging markets is hundreds of years old, the idea got a big push when the Soviet Union collapsed thirty years ago. Seemingly, this event ended one of the 20th century’s great policy debates decidedly in the direction of free markets. New capital markets opened up and investors envisaged markets that could provide both a positive return and diversification.

Yet, the question over the optimal political structure remained, largely between what Karl Popper (George Soros’s teacher) described as “open” or “closed” societies. Popper traced the debate back to Plato, who put more faith in rule by an enlightened few as opposed to giving the masses a say. Now these closed authoritarian structures appear to be tightening their grip in a way that is negatively impacting asset pricing and prioritizing domestic politics over capital markets.

I want to believe that open, flexible systems will prevail. The Russians I was with seemed to be largely making the same bet. At the same time, no one has ever tried to administer populations of this scale. When the US was founded, the population was roughly 4 million and of those only about 25% could vote. I’ve allocated a modest part of my portfolio to emerging markets. I need to think about it a bit more, but going forward this emerging market allocation may become even smaller even though the developed markets are, as traders say, expensive.