Not investment advice.

We are going to get a tightening in monetary policy, which is bad for assets. Inflation, as shown below, is around 4% in the US and 3% in Europe and is going higher due to the war in Iran and the resulting higher energy prices. It is increasingly clear that whatever resolution comes in Iran will take a long time, so oil prices remain elevated.

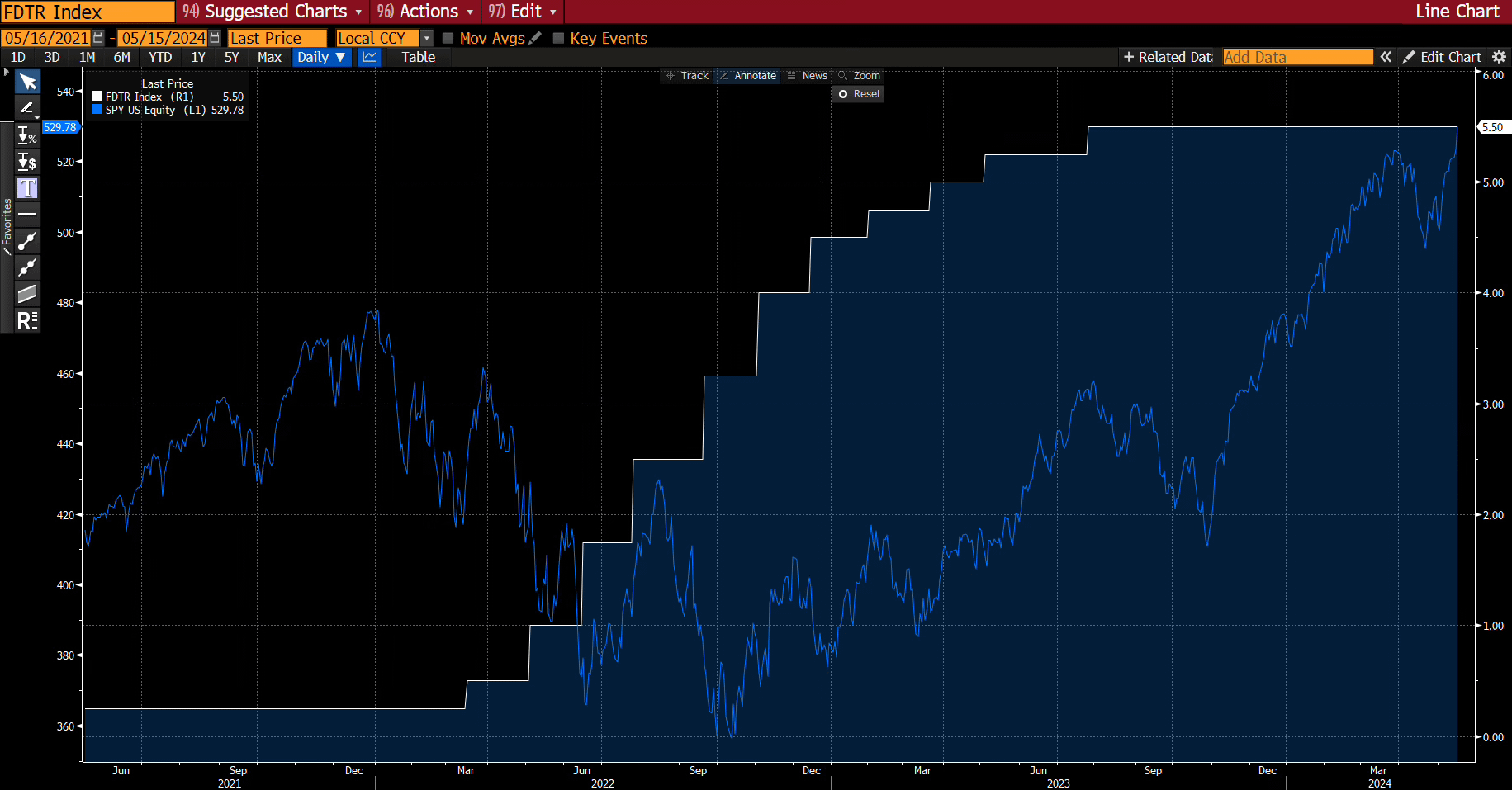

Tightening is generally bad for assets. Below I show the S&P index alongside the Fed Funds rate in 2022. Stocks fell around 15% the last time this happened.

Tech stocks may well correct but will go back up because we are in a productivity boom and

a) prices are rising at the same time as earnings, so stocks aren’t yet that expensive,

b) U.S. households keep buying, and

c) some managers are short indexes and get squeezed, so they buy to cover, driving prices up.

Bonds go down, however, because:

a) nominal growth is around 7 percent while bond yields are well below 5 percent,

b) households don’t buy as many bonds as they do stocks,

c) the government is running a big budget deficit,

d) the tariffs were judged illegal and the government now needs to refund the revenue it collected,

e) the US is in a war with tactical victory but strategic defeat, which requires yet more money,

f) the new Fed chief is probably reluctant to hike rates, boosting the risk premium on longer-dated bonds amid an increasing lack of confidence in US institutions (like what happened to UK bonds), and

g) capex booms require debt.

Currencies in the short term will be driven by oil and the Fed. Elevated oil prices are bad for the euro and yen but good for Brazil and Norway; a Fed tightening shifts the pressure to more dollar bullish. Tightening is generally bearish for precious metals like gold, silver, and copper. European central banks are already discounted to tighten, but in 2026 the Fed is not.

This document is strictly confidential and is intended for authorized recipients of “A Letter from Paul” (the “Letter”) only. It includes personal opinions that are current as of the date of this Letter and does not represent the official positions of Kate Capital LLC (“Kate Capital”). This letter is presented for discussion purposes only and is not intended as investment advice, an offer, or solicitation with respect to the purchase or sale of any security. Any unauthorized copying, disclosure, or distribution of the material in this presentation is strictly forbidden without the express written consent of Paul Podolsky or Kate Capital LLC.

If an investment idea is discussed in the Letter, there is no guarantee that the investment objective will be achieved. Past performance is not indicative of future results, which may vary. Actual results may differ materially from those expressed or implied. Unless otherwise noted, the valuation of the specific investment opportunity contained within this presentation is based upon information and data available as of the date these materials were prepared.

An investment with Kate Capital is speculative and involves significant risks, including the potential loss of all or a substantial portion of invested capital, the potential use of leverage, and the lack of liquidity of an investment. Recipients should not assume that securities or any companies identified in this presentation, or otherwise related to the information in this presentation, are, have been or will be, investments held by accounts managed by Kate Capital or that investments in any such securities have been or will be profitable. Please refer to the Private Placement Memorandum, and Kate Capital’s Form ADV, available at www.advisorinfo.sec.gov, for important information about an investment with Kate Capital.

Any companies identified herein in which Kate Capital is invested do not represent all of the investments made or recommended for any account managed by Kate Capital. Certain information presented herein has been supplied by third parties, including management or agents of the underlying portfolio company. While Kate Capital believes such information to be accurate, it has relied upon such third parties to provide accurate information and has not independently verified such information.

The graphs, charts, and other visual aids are provided for informational purposes only. None of these graphs, charts, or visual aids can of themselves be used to make investment decisions. No representation is made that these will assist any person in making investment decisions and no graph, chart or other visual aid can capture all factors and variables required in making such decisions.

The tightening logic is clean and the bond case is especially sharp — point (f) about the new Fed chief's reluctance creating a risk premium on duration is the kind of thing most macro commentary skips over.

One layer I'd add on the "resolution will take a long time" point, since it feeds directly into the inflation trajectory you're mapping.

The physical constraints on Hormuz normalization aren't vague — they're sequential and measurable. Mine clearance takes 6+ months, and Iran laid a second round of mines in April so the clock keeps resetting. After clearance, insurance reclassification operates on quarterly committee cycles at the P&I clubs — zero of twelve have reclassified and the process can't be politically accelerated. Stack those timelines and you're looking at 8-10 months minimum from the day the last mine is cleared. Not from today.

That timeline changes the inflation math. The oil price input into your inflation chart isn't a temporary spike that fades with a ceasefire — it's a sustained elevated input with a specific minimum duration. And the transmission isn't instant. Fuel costs hit in 1-2 weeks but freight repricing takes 4-8 weeks, industrial input costs follow at 4-12 weeks, and agricultural pass-through runs 12-26 weeks behind that.

Which means even if oil peaked today, the inflation waves you're flagging have multiple stages still in the pipeline that haven't arrived yet. The tightening case isn't just about current inflation — it's about the inflation that's already locked in but hasn't shown up in the data.

That makes your duration call on bonds even stronger than your analysis suggests.