What I'm Seeing

THIS IS NOT INVESTMENT ADVICE. INVESTING IS RISKY AND OFTEN PAINFUL. DO YOUR OWN RESEARCH.

Investing is never easy. It sometimes looks easy in retrospect when an index like the NASDAQ goes up 30%, but a year ago that was not obvious and what will happen a year from now is not obvious. To navigate, I identify objective facts or likely theses that, like buoys, help me paddle through whatever waves, fog or calm comes my way.

Here are the buoys I see.

The global economy is growing, but growth is uneven. The key distinction between places that are growing and those that aren’t are a) growing workforces (via immigration) b) lax fiscal policy c) proximity to AI and d) tied into Western as opposed to Soviet alliances. You are either inside that circumference or outside. Similarly, certain industries are churning out profits (AI) while others (like defense) are not nearly as profitable.

More specifically:

The US will probably grow around 5% nominal next year. That’s fast. This is because the US is at the epicenter of the circumference I described above. Could we have above average growth and lower inflation? Maybe.

Europe is not growing much and Germany isn’t growing at all. Europe is hurt by bad demographics, China export dependence, expected tariffs, and an ossified administrative bureaucracy. There is one global European AI company in the European index (ASML) and even this company has a lot of sales to China.

In addition to unfavorable demographics and brain drain, China is hurt by a large (we don’t know how large) debt overhang, vague macroeconomic policy, and self-destructive alliances with Russia and Iran. Xi’s politics scare off capital. At some point the economy may become bad enough that China will apply meaningful stimulus, like issuing new debt to buy back the bad debt and then printing money to buy these new bonds, but it took Japan over 10 years of deflation and watching the US print after 2008 before Japan’s policy really began to change. The risk is China talks about doing stimulus but doesn’t actually do that much. We are watching carefully.

Japan is breaking out of a 35-year deflationary debt spiral due to years of stimulative monetary and fiscal policy, a weak currency, and higher labor participation. This is under appreciated. Japan realized there is now a fourth phase of life. It used to be that there was childhood, adulthood and old age. Now there is a third stage — no longer young, still capable. It runs from 50 to about 80. We’ve never had this cohort before. When I was a kid, 60 was old. Now people lift weights and want to stay engaged. That’s why Bill Belichick went back to coaching.

EM is mixed. Parts of India are in a boom, Brazil is in a debt spiral and Russia is un-investable. Overall, EM is EM in part because it is often unfavorable for investors. For instance, the return of Chinese stocks has been poor in part because companies there issue a lot of shares while, by contrast, in the US, companies buy them back. The first increases supply, the second decreases it. Now China is saying it wants to change this equity culture. Maybe it will change. Again, we are watching.

This macro is made of micro. In the US, everything connected with AI is exploding but small businesses exposed to higher interest rates or the lower ends of the income distribution who are no longer getting stimulus checks are struggling.

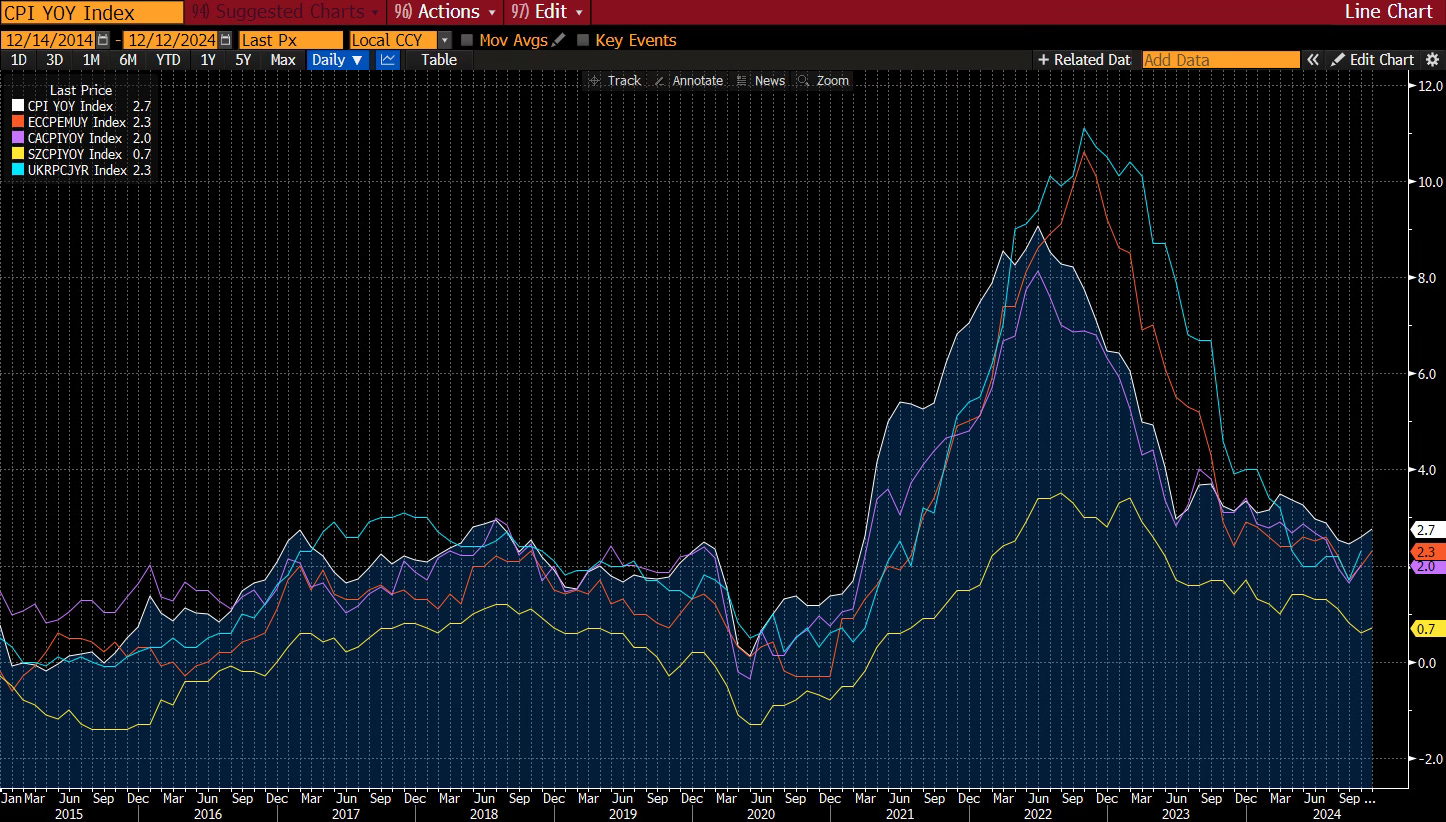

Inflation is reverting back to where it was pre-Covid, with the exception of those countries (US and Japan) running easy fiscal policy and with increased labor participation. This makes sense. What’s fundamentally changed since Covid? First, better technology, which is deflationary. I suspect in those places that are not running stimulative fiscal, inflation will end up right back where it started, maybe even below. Second, higher interest rates, rates high enough to essentially curtail private sector borrowing in places like the US.

AI will change a lot of things, but no one, including the people who are doing the AI investing, understand exactly what the implications are. For instance, I just spent a lot of money on legal fees to set up a new company. There are a lot of start-ups now that allow AI to do this. How long until such documents are acceptable and common? What does it do to lawyers’ salaries? What about the barriers to entry in a new company? Much of that will be known in the next few years but many companies are already experimenting with using AI in their day-to-day. I do at Kate Capital. The inflation there is is in services, and some of these services can be disrupted by AI. That is how we get lower inflation and faster growth. Maybe.

The “system” has unusual characteristics. Those people who are close to the most revolutionary changes are standing on cash geysers that can explode at any moment and turn what was once a geeky computer guy or gal into someone worth hundreds of millions of dollars. But this same technology can be used to entomb a health care interface with bots that deny you care, perhaps leading the psychologically fragile into homicidal rage. It was interesting that Thursday President-elect Trump spoke out against automation. This is like speaking out against electricity but clearly the man knows how to touch the right nerve in his listeners.

Global conflict is severe and bloody. In the time I sat at my desk today, something like 2,000 more Russians were maimed or killed. Probably a few hundred Ukranians. One upsdie of this conflict is that it may (repeat may) persuade China that the best bet is to psychologically torture Taiwan as opposed to actually fight to force re-unification. When China invaded Vietnam, it retreated after 29 days. Russia has invaded many countries and territories over hundreds of years. At the higher level, Iran, Russia and China are fighting a losing battle because they are on the wrong side of wealth generation. War is expensive and you need the magical elixir of fast growth to finance it. That’s not shown over a day or even a year but over 10 years it is evident. This is why Putin’s negotiating position, absent nukes, is weak. In the West, no one knows how to both have the spectacular wealth generation but also not to have the huge wealth inequality. That’s been an issue since the Industrial Revolution, it is just more acute today because of the nature of the technology.

And yes, shameless book plug: