Our Stock Market Addiction

Our Stock Market Addiction

Incentive Distortion

Dude, everyone is doing it, just re-register your company as an C-Corp and put out the call for money. In this environment, why not?

I was speaking with an entrepreneur. He has a disruptive idea backed by venture money. Before a company goes public, there is an eco-system of lenders who fund early-stage companies in the low odds hope one of them will become the next Apple. (My company, Still Press, is an LLC). The higher stock prices rise, the more willingness there is to bet on early-stage ideas. This now looks excessive.

Many things are magical in moderation and terrible in excess. Alcohol, food, exercise and work can all become addictive. Addictions organize reality, create drama, make us want more and spread wreckage. The stock market now meets this standard.

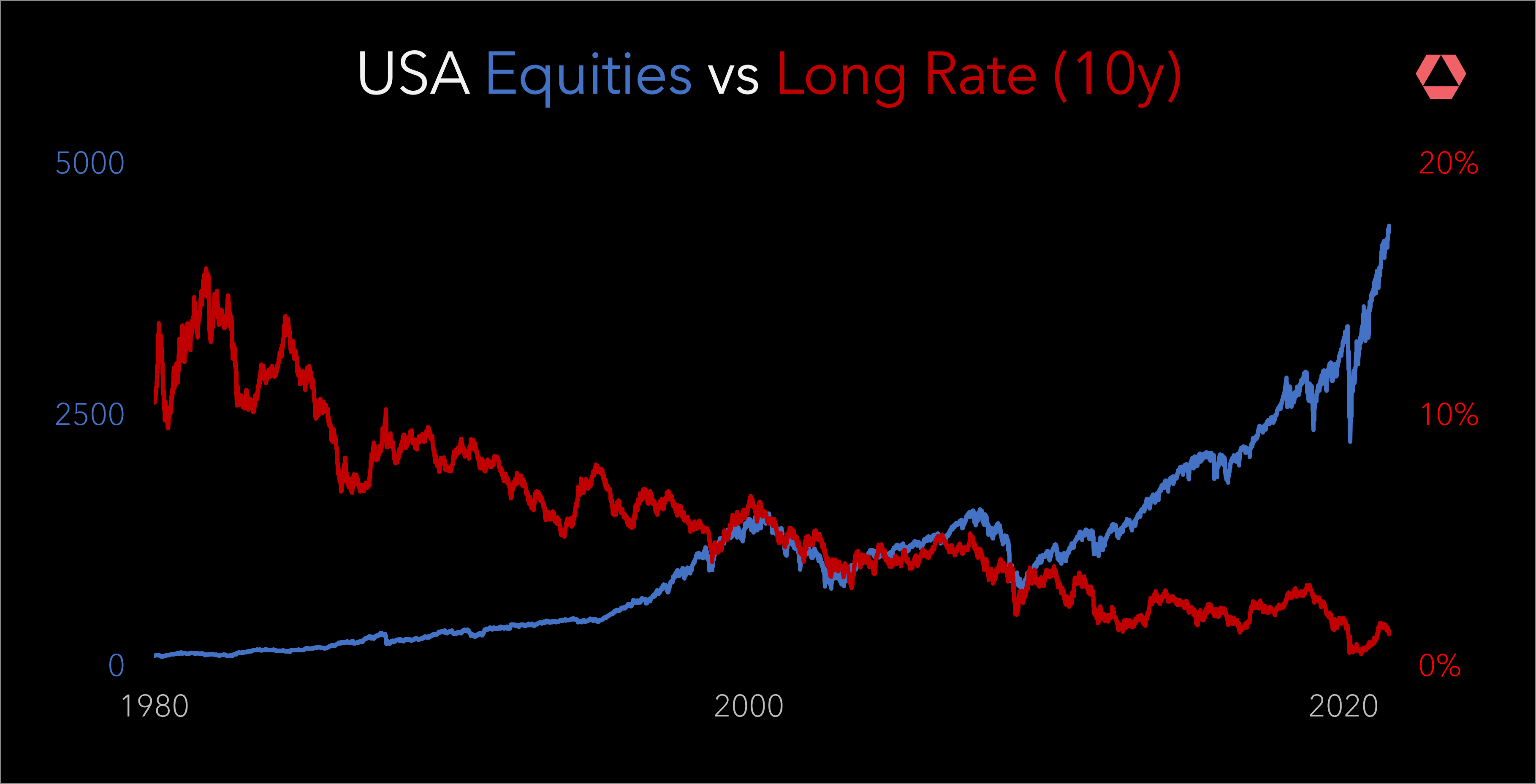

In terms of economic policy, the stock market is now having an outsize impact. Some context (finance people skip). Financial folk focus on prices, cotton prices relative to Apple stock, buy low and sell high. The process that sets each price is intricate, passing through many pipes and spigots, though ultimately the money comes from just one place, the central bank.

Stocks typically crash when prices are high and conditions shift quickly, often pre-ceded by a reduction in money printing. Almost no one likes it when stocks crash. Everyone who owns a stock gets poorer. No Fed chief wants their name associated with a big crash, the way President Herbert Hoover’s name is associated with the 1929 crash. As a result of both the economic impact and, I suspect, reputation legacy, in recent decades each Fed chief has been quick to act when stocks fell sharply in 1987, 2000, 2008 and 2020.

They stop a crash by printing money. When printed money goes into the economy it creates inflation. When printed money goes into stocks it creates a bull market. Because we have had repeated crises, we have had repeated easings. Interest rates, now zero, are the cost of money, meaning borrowing money is free. The price of one—stocks—is tied to the price of the other—money.

Going forward, we are in a delicate spot. Many (but not all) measures of US stock prices (none of them precise) suggest the US stock market is very expensive relative to average. The very success of past money printing has increased household sensitivity to the stock market going forward, though some people own more stocks and some less. While I don’t see an obvious catalyst in the short-term, I also recognize even a modest money printing reduction could have an outsize effect, driving stocks sharply lower.

In terms of business, the stock market is creating powerful incentives. When you start a business, the big challenge is cash flow. You have an idea but no profits. A loan is onerous. If the new business fails (and most do) the entrepreneur is still the hook for the debt. No bueno. If you issue a stock and the company fails, the entrepreneur owes nothing.

Today’s stock frenzy is a bonanza for start-ups. If everyone wants to buy a stock, why not issue it? Of course, this process funded many incredible companies. The software I am writing this with, the computer I use, the high-speed connection, etc. are all a part of this dynamic. But with the stock market and stock options this frothy, it creates an incentive structure that makes it hard to discriminate a good business from bad and sucks talent into any sector that can issue stock, even if that is not a good use of society’s limited talent resources.

Yes, central banks have good short-term reasons for printing. We are in a pandemic; more refined estimates suggest more than 10 million dead! If now isn’t an emergency, what is? But this policy comes with collateral damage.

Entertainment is another element of the addiction. Multiple cable TV stations make their money by reporting breathlessly on what is happening with the market. If you think about it, it’s odd. The stock market helps companies, which might last a generation each, to raise money. Why update it like a tennis match? Retail Apps that allow for even faster trading of stocks further turn the process into a game.

In terms wreckage, we are living in a massive asset values run up. The next generation needs to buy these assets from us, the people that own them. The prospect for the return of doing so likely is not good. This quixotic chart below puts this in perspective, our generation is just a moment in time. See my post, Letter to a Young Person, for thoughts about what to do.

This stock frenzy will either ebb or crash when the Fed reduces the money they are printing. Maybe we just go sideways as opposed to down. In any case, that is an issue for 2022 and 2023. I’m long stocks as part of my asset allocation, but only hold about 10%-15% of them in the US and I maintain hedges in my portfolio to help reduce the pain when the Fed eventually shifts behavior.

If you enjoyed this post, please share it.

NOTE to readers: I will not be publishing in August. Also, THE ABOVE IS NOT INVESTMENT ADVICE, I AM SHARING THOUGHTS.