For those new to Things I Didn't Learn in School, a brief explanation. We air a podcast twice a month and a weekly written note. The two are different, but inter-relate. The weekly note is usually about a macro-economic or investment topic, very broadly defined. The podcasts are micro, individual life stories. Our next episode airs October 27. Each helps illustrate the other. More about what we (and it is a team) are up to, is here. If you are less familiar with investing, The Lull, which includes editions #32, #33 and #36 is a good place to start.

It’s so obvious it’s ours, said my companion, smiling genially.

I was at lunch in Beijing pre-Covid and my companion was describing a recent trip he had taken to Taiwan. His view represents a common one on mainland China.

While only Chinese President Xi knows if he intends to take Taiwan, I’ll take his word for it. “The historical task of the complete reunification of the motherland must be fulfilled, and will definitely be fulfilled,” he said earlier this month. Even if you put aside any consideration of civil liberties, if Xi takes this step, he will likely meaningfully slow future Chinese and global growth.

The basic point: taking Taiwan would be economically costly for China itself and in that sense self-destructive.

Countries invade each other. Often it is rich country (like the US) invading a poorer country (like Iraq). The list of countries that are poorer invading countries that are richer is shorter. Per capita GDP in China is about $10k, versus about $30K in Taiwan. A parallel is perhaps the Soviet Union’s 1956 attack on Hungary.

While I am not a military expert, I spoke with some. The consensus was that a) the US would not put soldiers on the ground to defend Taiwan and b) the Taiwanese themselves are split on the merits of dying in battle. Still, taking Taiwan by force would be a major breech of the status quo.

A notable difference between territorial disputes now and in previous centuries is the relative sophistication of financial markets. World powers borrow mostly in their own currency and their lenders include global pensions and households. Shifts in market pricing and economic statistics provide objective facts to assess the cost of a specific policy choice.

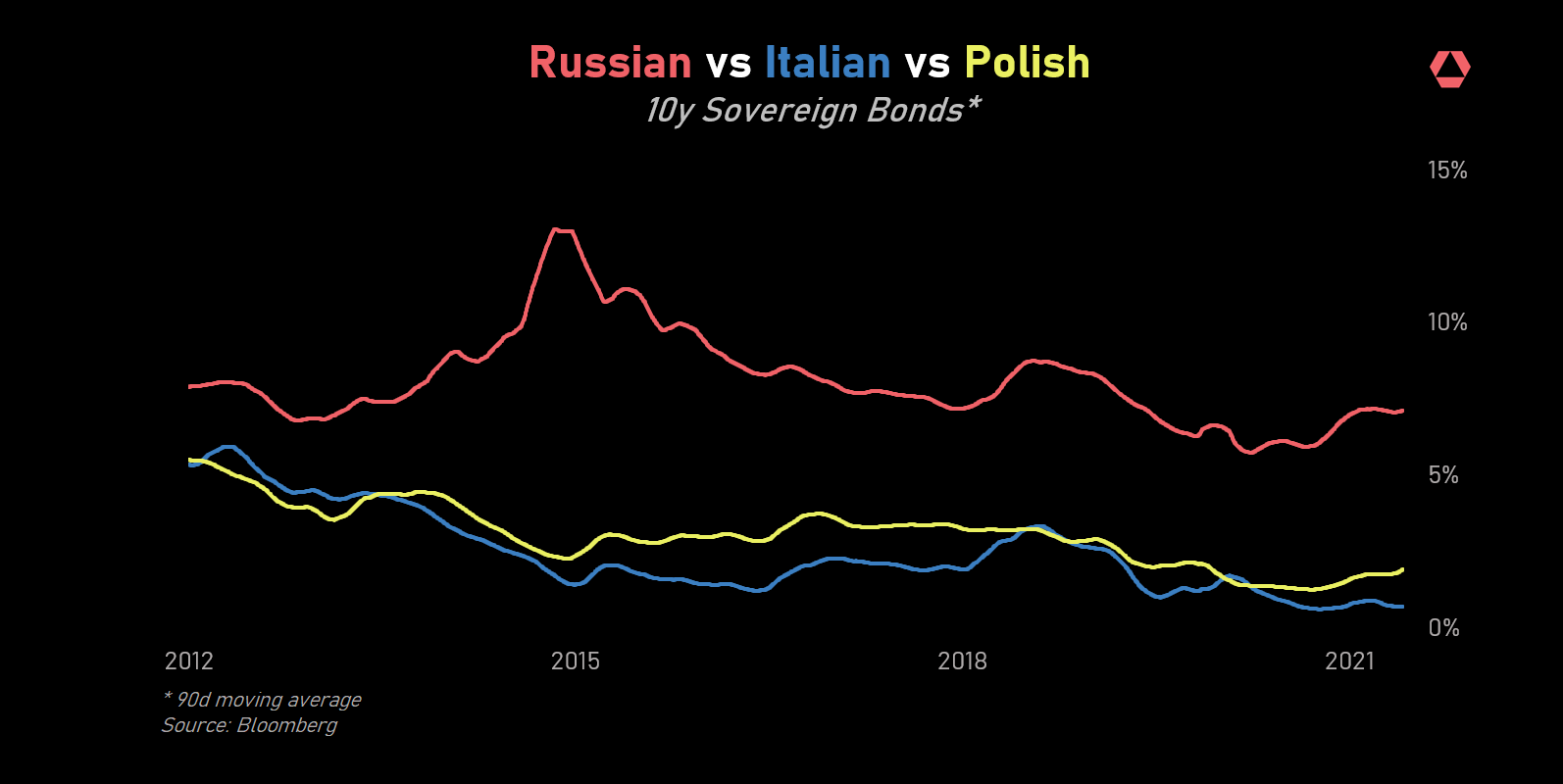

Both Russia and the US offer case studies. By cost, I do not mean the obvious cost in terms of lives lost or direct military spending. Instead, I mean the economic growth that would have occurred had these conflicts been avoided. When Putin invaded Crimea in 2014, the ruble fell sharply, the cost of imports soared and inflation rose.1 In response, the central bank raised interest rates and the cost of capital increased, as the chart below from Rose illustrates. I looked at Poland (a former member of the Soviet bloc) and Norway (an oil exporter) for comparison.

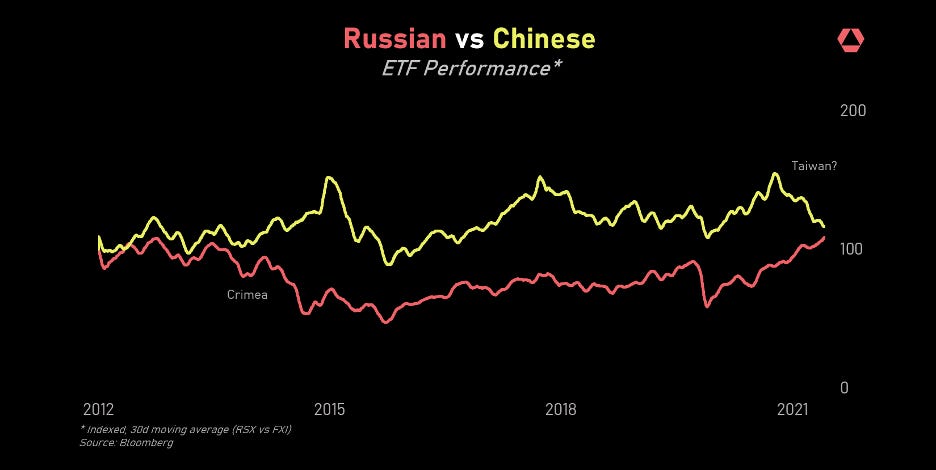

Growth is spending. Spending comes from income and borrowing. As the cost borrowing rises, credit demand slows and economic growth suffers. Following the credit market tightening, from 2014 to pre-pandemic, the Russian economy grew about 1% a year. Below shows the economy measured in dollars. By this measure, the economy is actually smaller now than in 2014.

By contrast, over the same period a neighboring economy like Poland grew roughly 4%. China’s growth was even faster. Norway also grew faster than Russia. While these calculations are not precise, this suggests by invading Crimea Russia forfeited roughly $300-$500 billion of output.

In the US invasions of Iraq and Afghanistan the issue was less a disruption of capital and more a misallocation. The invasions cost roughly $8 trillion in direct costs.2 Essentially, the US developed infrastructure abroad, not home. Each dollar invested in infrastructure has a “multiplier” effect, meaning one dollar spent on a railroad creates additional dollars spent on steel, electricity, etc. Calculations around the multiplier effect on infrastructure vary, but a low estimate is 1.5. This suggests the US forfeited $12 trillion of domestic economic growth.

The economic calculations with China are different. Unlike the ruble or dollar, the yuan is not freely convertible. Given these capital controls, if Xi takes Taiwan, the impact on Chinese bond and currency markets is likely to be more muted. Instead, the impact is likely to be on productivity.

Since it opened up in the early 1980s, China grew rapidly by opening up and squeezing modernization undertaken by other countries into a shorter time span. Now China faces challenges similar to other major economies—too much debt, unequal growth and disruptive technology. The basic question—should China tackle these problems by opening up further or isolating?

If Xi invades Taiwan, it will mark a definite additional step toward isolation. Foreign direct investment will likely slow, institutional investors will back away from Chinese capital markets and China’s integration with the rest of the world will ebb, as it has many times over its long history. Based on examples in the US and Russia, this impact is perhaps around 20 to 60 basis points of GDP growth a year, or $600-$700 billion of Chinese GDP over the next decade. It doesn’t seem like a great bet, but then again, Crimea and Iraq fail the same test.

Yes, there were other dynamics at work. Russia’s primary source of income is raw materials. For reasons largely unrelated to Crimea, at this time oil prices fell from around $100 a barrel to $50. But weaker growth is a deflationary shock, so the distress in the bond market was primarily due to Crimea, not commodities.

https://watson.brown.edu/costsofwar/papers/summary

Thanks to Paul for the observation, yes, they are calculating the "political account", not the "economic account". The former means arbitrary, willful, and irrational.