Welcome! If this was forwarded to you, you can read what I am up to here or sign up to receive the free or paid version below. This week is both an essay and a Mother’s Day podcast with my amazing wife Marina, which you can hear here.

The future is always murky, the past obvious by comparison. The degree to which the future becomes miraculous or awful depends on how well each generation discerns and invests in that murky future. Miraculous looks like mRNA vaccines, 1G internet and driverless electric cars. Awful are Russia’s collapsing living standards.

Until relatively recently, the murky future was supposed to be carbon neutral, cash flow negative tech start-ups. But that vision turns out to have been wildly misguided. Inflation is high and tech workers are getting sacked because we invested too little in oil and natural gas and too much in tech. This miscalculation was exacerbated by easy money, Covid and Ukraine. Below, courtesy of Rose, is a picture of the “capex,” basically investment, of the two sectors. Oops.

In popular culture, Wall Street is often portrayed as the villain. While there are unsavory people on Wall Street, the ecosystem itself provides an invaluable service—directing capital toward the future.1 But doing so is more art than science despite the amount of math types involved. This has implications for central planning and instability.

Central planning doesn’t work well because trying to figure out what tomorrow’s miracle inventions should be is hard even in a system where people are incentivized to do just that. In the US, Katalin Kariko, whose research led to the mRNA vaccines, was refused grant after grant and demoted by the University of Pennsylvania!2 How likely is a Politburo member to see what the venture/biotech/academic community missed? Yes, Chinese central planning lifted hundreds of millions out of poverty, though this was more catch up following decades of chaos (Civil War plus Cultural Revolution) using a relatively clear development template. Regarding instability, the murkiness of the future means it is inherently difficult to value a company––either to work in or to own a part of. This means the likelihood of losing a job or money on an investment in any particular sector is high.

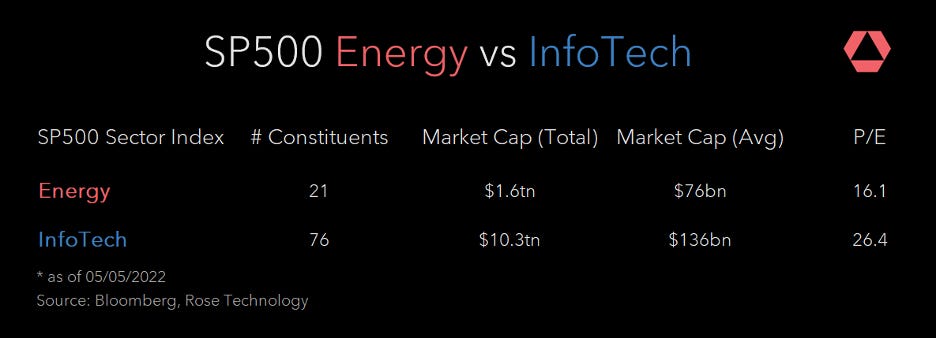

Haliburton Vs. Netflix

When you work for a company or invest in its stock, you are renting out your labor or your money. The goal is to rent out either for as much as possible. Counterintuitively, the higher the price of the company, typically the less you receive for rent. As prices on tech soared and those on dirty energy companies plummeted, the rent received tilted more and more in favor of energy and away from tech.

Today’s pricing shows how much and how quickly perceptions can shift. A one-time darling like Netflix is down 70% this year and a company that helps pull oil out of the ground, Halliburton, is up 60%. One stock market, but two very different stories.

In part this pricing is because processing one-off “shocks” is hard for humans. We are designed to spot patterns, which requires repetition. To make sense of the pandemic, we looked to 1918, but failed to anticipate the vaccines or China’s zero Covid policy. In the chaos, the price of oil actually went negative. Now there is Ukraine, which creates the risk of a nuclear conflict. How do you price that?

Each shock shifts hundreds of billions of dollars. Wall Street doesn’t do “reverse” very well. The machine is set up to sell securities around a story to investors that hold them and benefit from future price rises. Wall Street is not incentivized, by and large, to warn investors or build portfolios to protect when prices fall. That’s why most portfolios are down so much this year.

More Pain Ahead

Going forward, we are likely in a negatively self-reinforcing dynamic that will last for a while (investment implications a bit lower down). The shortage of oil due to underinvestment is exacerbated when countries cut their demand for Russian oil. Consumers need about the same amount of oil, but supply is less so price rises.

Oil is inflation, or at least a big part of it, which is what the chart below shows.

Oil is in your heating and driving and the cost of every Amazon delivery you get. This means the Fed now needs to tighten even more. Earnings will likely slow and PE’s likely fall as interest rates rise. As I showed last week, it isn’t difficult to see how stock prices could fall another 20%, though this is not investment advice. Plus, there is China’s zero Covid policy, which has further disrupted supply chains, which is also inflationary. The Fed can’t solve a supply-chain problem, so it needs to throttle demand.

We will hit bottom when prices cool. But this might take a while. For instance, re-routing energy infrastructure is likely to take a few years. This is both because building new facilities, like natural gas terminals in Europe, takes time and also because in the West there is resistance to new energy infrastructure. The example frequently cited is that Quebec has a surplus of hydro power but environmental opposition has prevented the construction of 192-mile transmission line through New Hampshire.3

Despite these facts, investors believe a much brighter future still awaits technology, perhaps because these companies have the possibility of creating something that is almost free—like the technology behind TikTok—that can reach billions of people. Said differently, rent is still lower in tech perhaps in part because the economies of scale are so alluring.

Russia Update & Mother’s Day Podcast:

The news from Russia is so bizarre it is difficult to process. Last week, Russia’s foreign minister equated Ukraine’s Jewish leader, Zelensky, with Hitler, adding the weird lie that Hitler also had “Jewish blood.”4 A chunk of Russia, including my mother-in-law, seems to have lost their mind. There is a tape I posted on Twitter (@paul_podolsky) of captured Russian soldiers calling their mothers, saying they managed to survive and that the whole attack is a waste. Their own mothers tell them to stop complaining and eliminate the “Nazis.” Propaganda works much better than I had ever imagined. My source in all things Russia is my wife Marina and I recorded a special Mother’s day podcast here.

Investment Outlook

How to navigate the dynamic I’ve described above? By doing things differently than normal. In practice